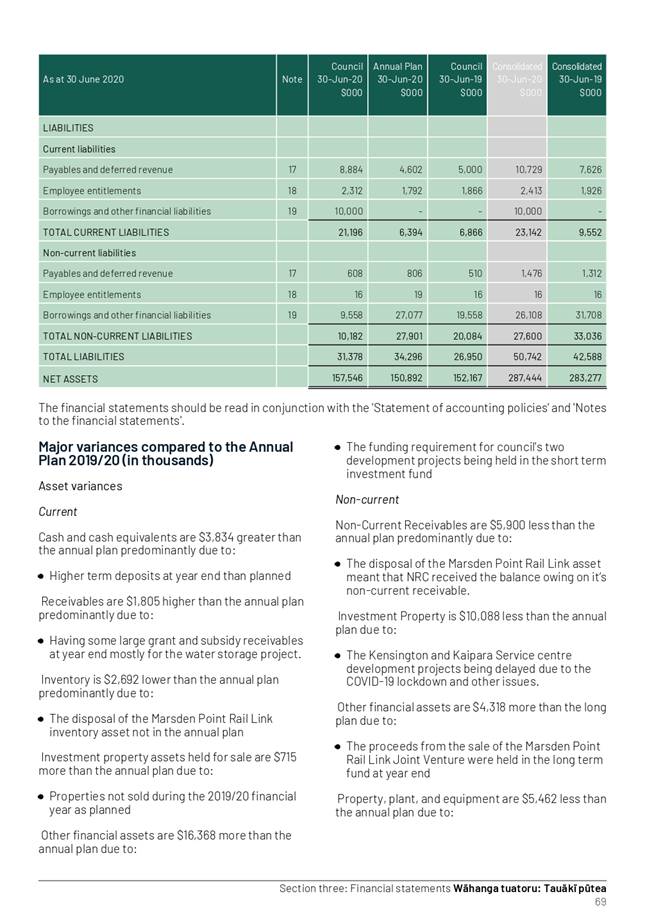

|

Audit and Risk Subcommittee Tuesday 6 October 2020 at 10.30am

|

|

|

|

|

|

Audit and Risk Subcommittee Tuesday 6 October 2020 at 10.30am

|

|

|

|

|

Audit and Risk Subcommittee

6 October 2020

Audit and Risk Subcommittee Agenda

Meeting to be held in the Council Chamber

36 Water Street, Whangārei

on Tuesday 6 October 2020, commencing at 10.30am

Recommendations contained in the agenda are NOT decisions of the meeting. Please refer to minutes for resolutions.

MEMBERSHIP OF THE Audit and Risk Subcommittee

Chairperson, Councillor Colin Kitchen

|

Councillor John Bain |

Councillor Amy Macdonald |

Councillor Joce Yeoman |

|

Ex-Officio Penny Smart |

Independent Financial Advisor Geoff Copstick |

Independent Audit & Risk Advisor Danny Tuato'o |

Item Page

1.0 Housekeeping

2.0 apologies

3.0 declarations of conflicts of interest

4.1 Confirmation of Minutes - 24 June 2020 3

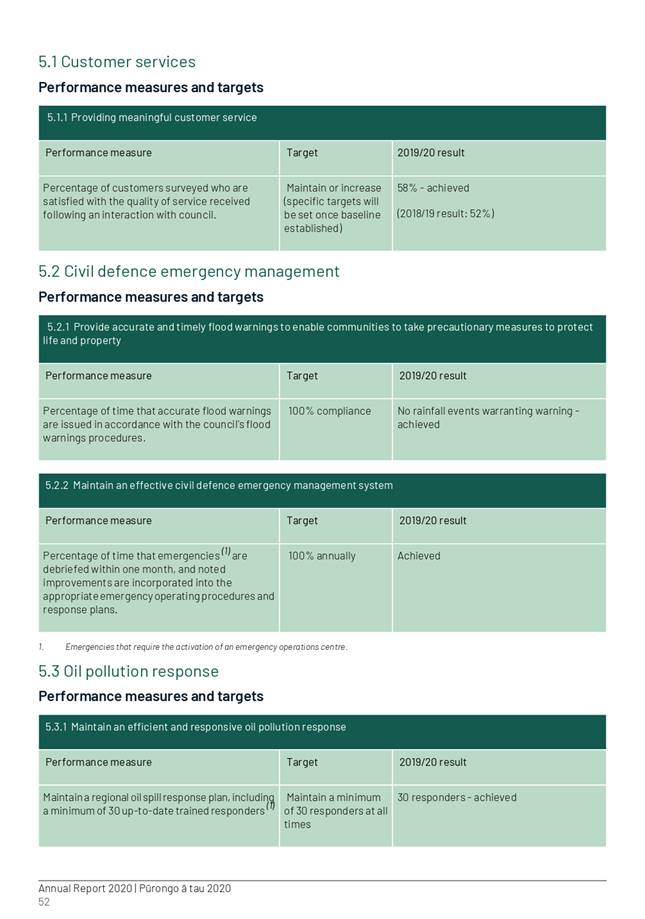

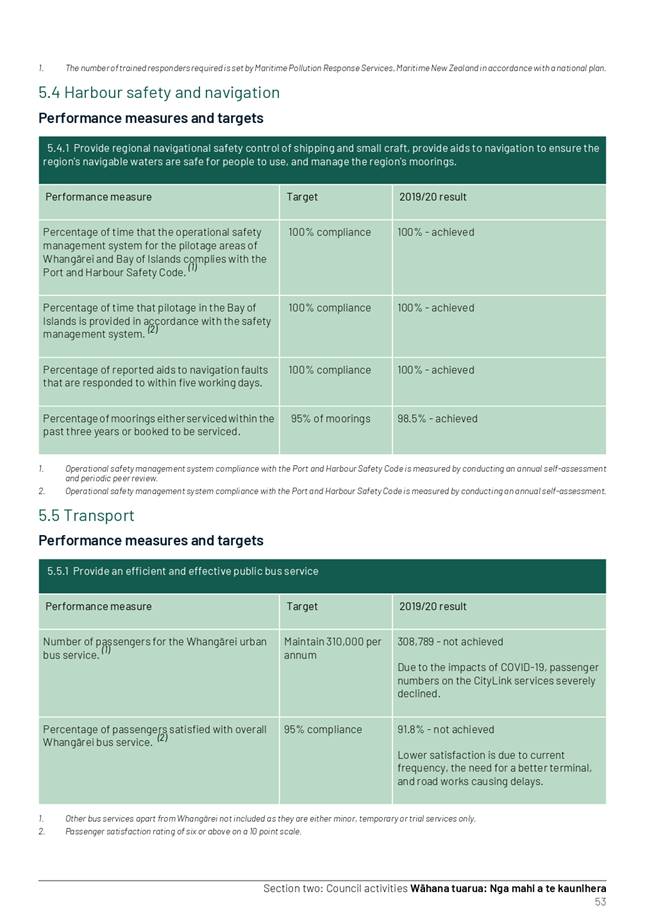

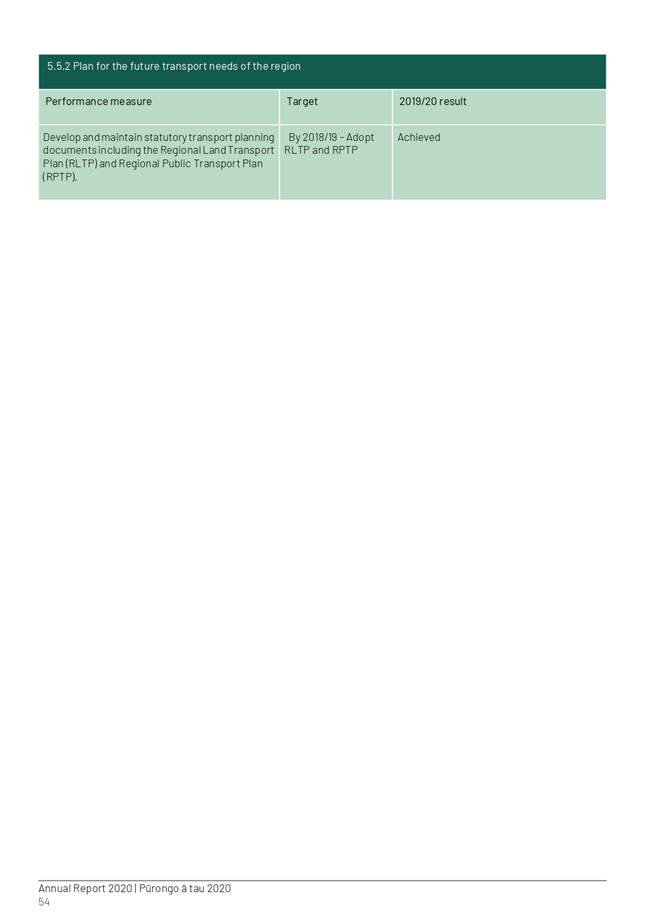

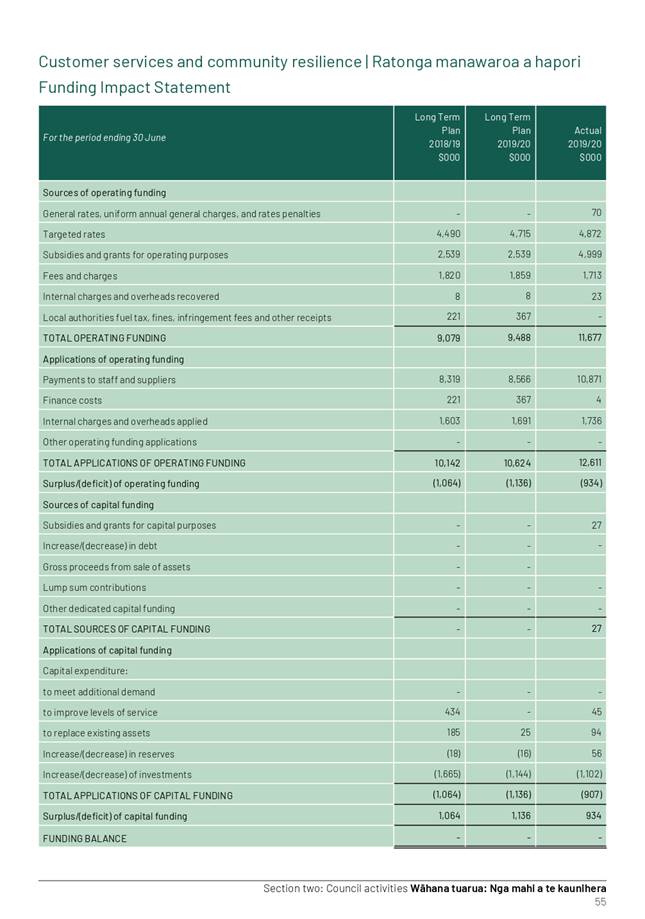

5.1 2019/20 Annual Report and Deloitte Audit Report 4

5.2 Risk Management Activity- Update 193

6.0 Business with the Public Excluded 212

6.1 Confirmation of Confidential Minutes - 24 June 2020

6.2 Up date form AON Insurance

Audit and Risk Subcommittee item: 4.1

6 October 2020

|

TITLE: |

Confirmation of Minutes - 24 June 2020 |

|

ID: |

A1358805 |

|

From: |

Judith Graham, Corporate Excellence P/A |

That the minutes of the Audit & Risk Subcommittee meeting held on 24 June 2020 to be confirmed as a true and correct record.

Attachments/Ngā tapirihanga

Nil

Authorised by Group Manager

|

Name: |

Bruce Howse, Group Manager - Corporate Excellence, |

|

Title: |

Group Manager - Corporate Excellence |

|

Date: |

|

Audit and Risk Subcommittee item: 5.1

6 October 2020

|

TITLE: |

2019/20 Annual Report and Deloitte Audit Report |

|

ID: |

A1362628 |

|

From: |

Simon Crabb, Finance Manager |

Executive summary/Whakarāpopototanga

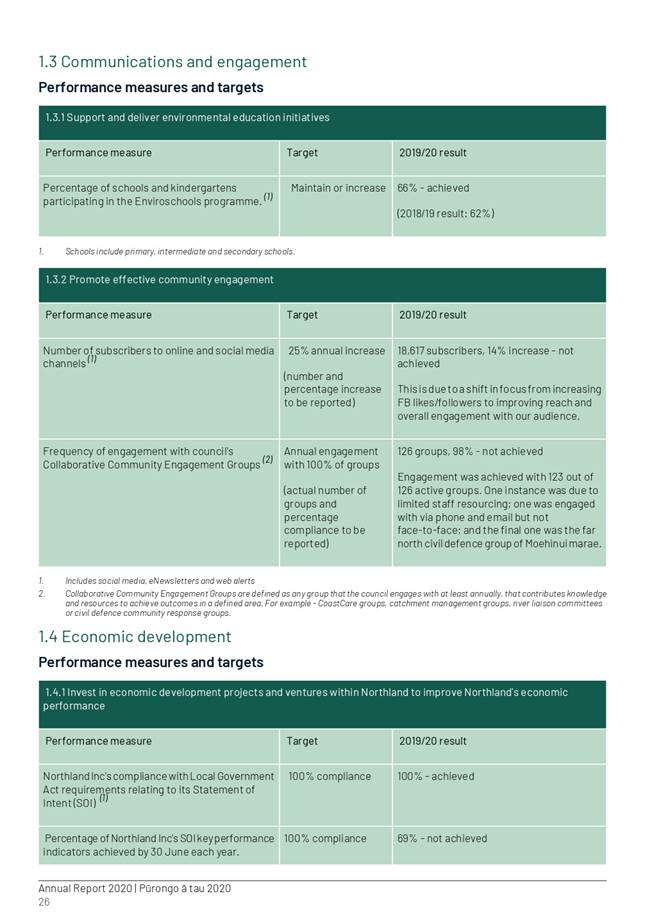

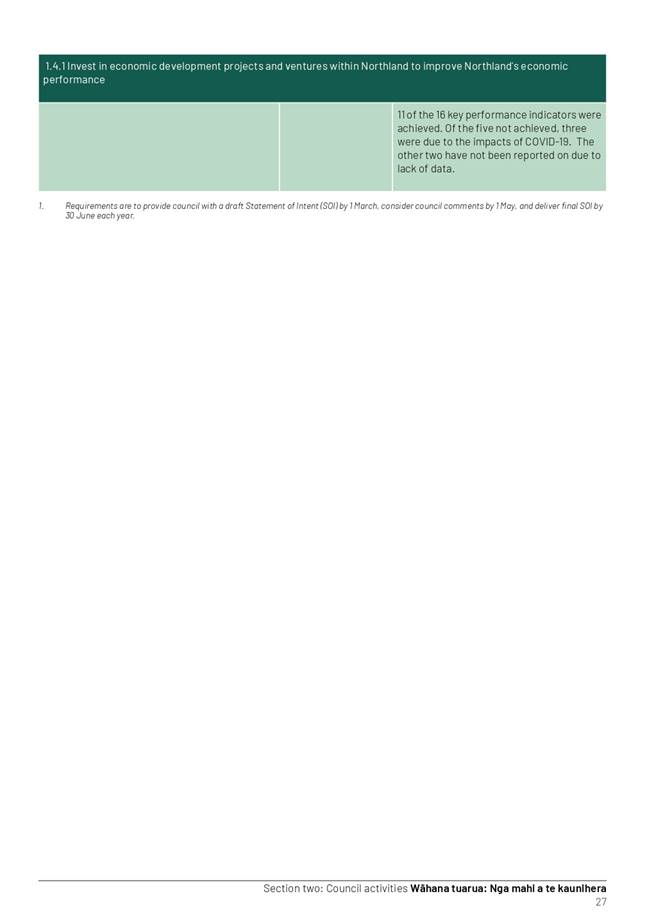

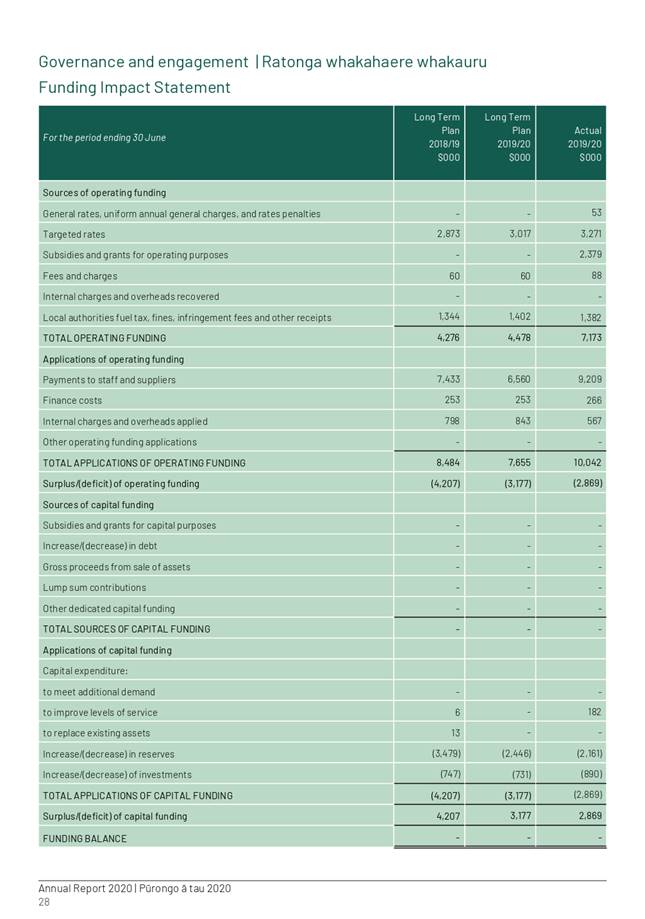

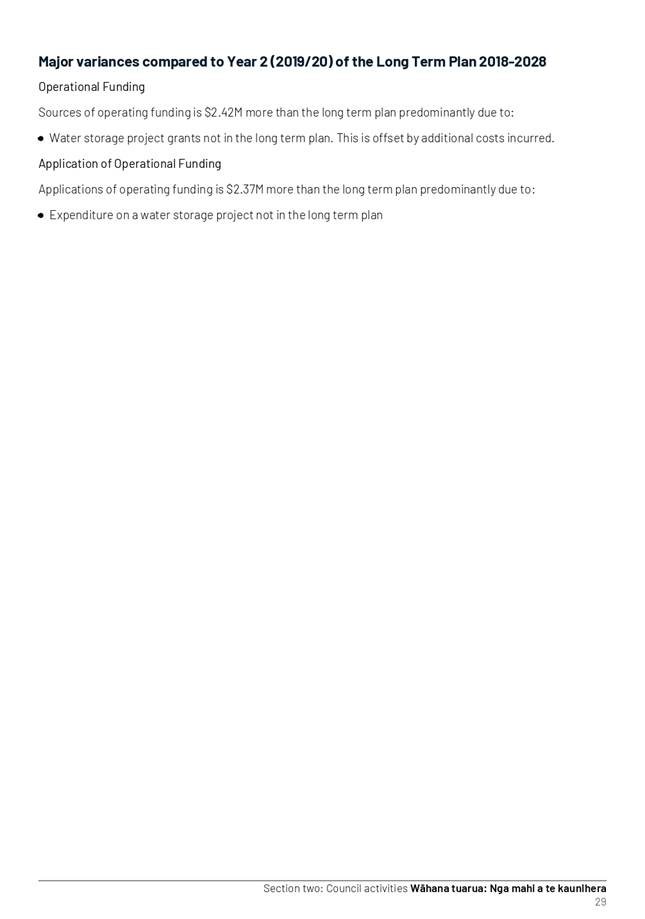

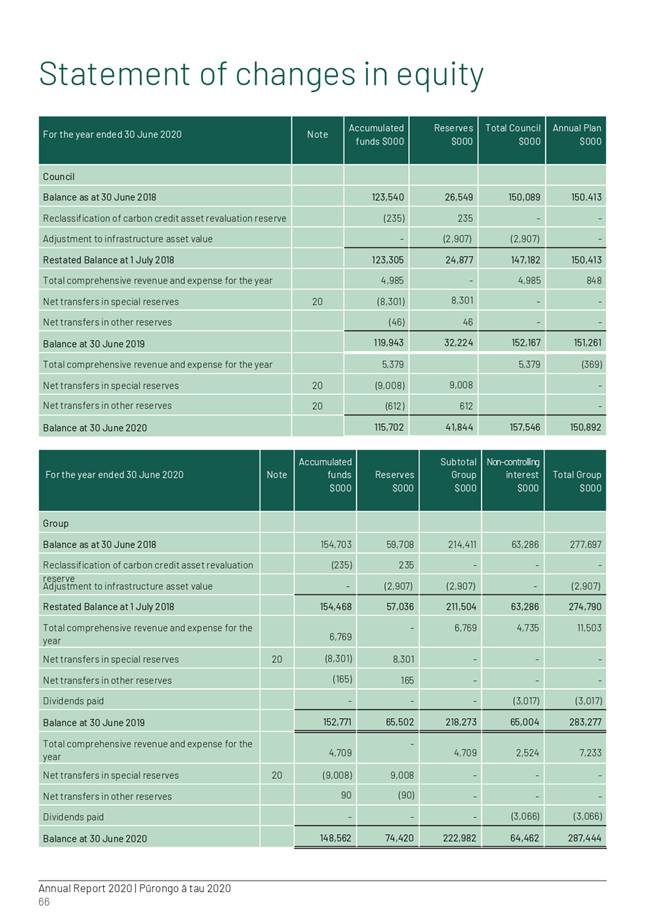

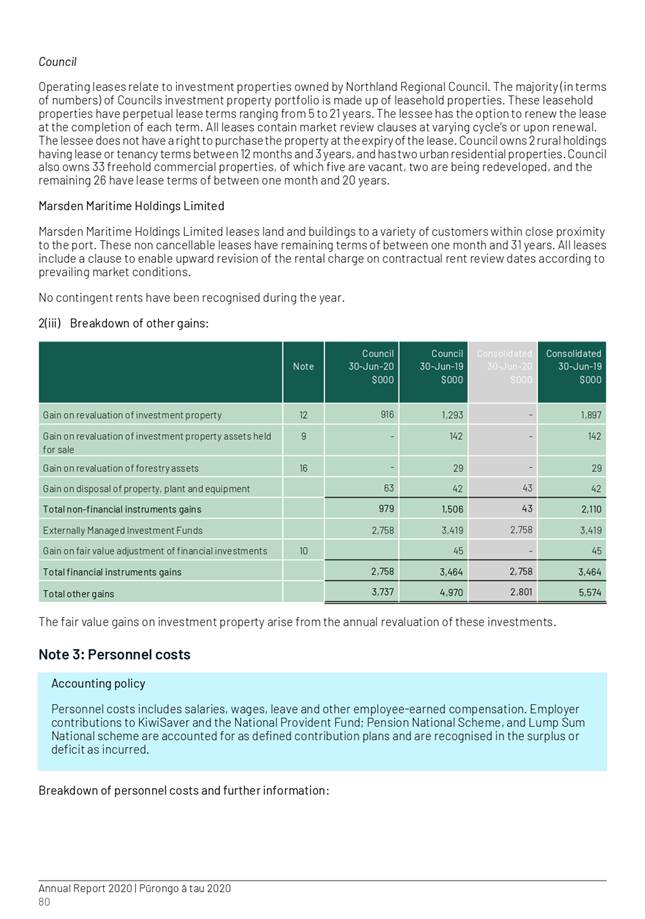

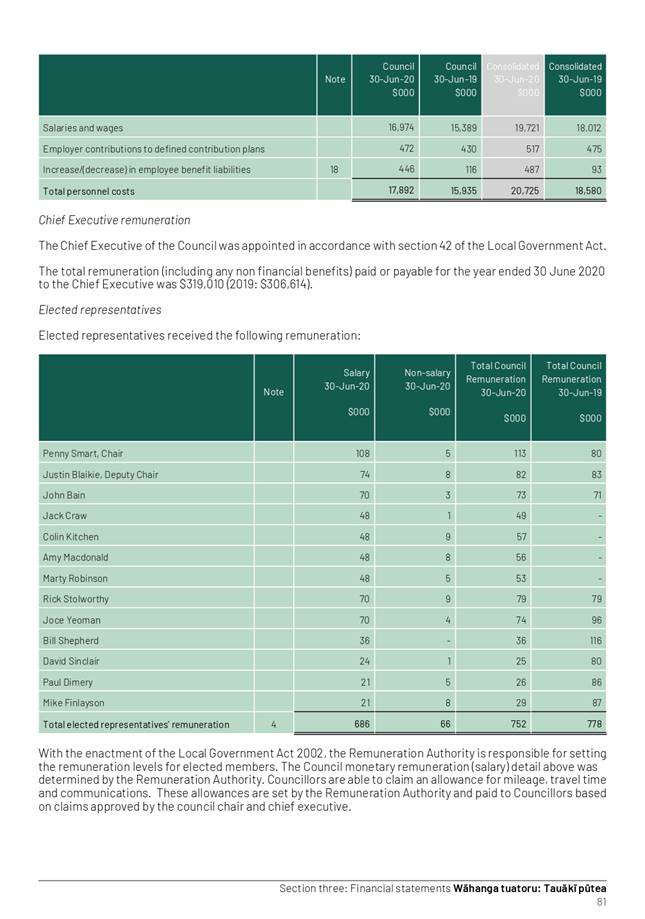

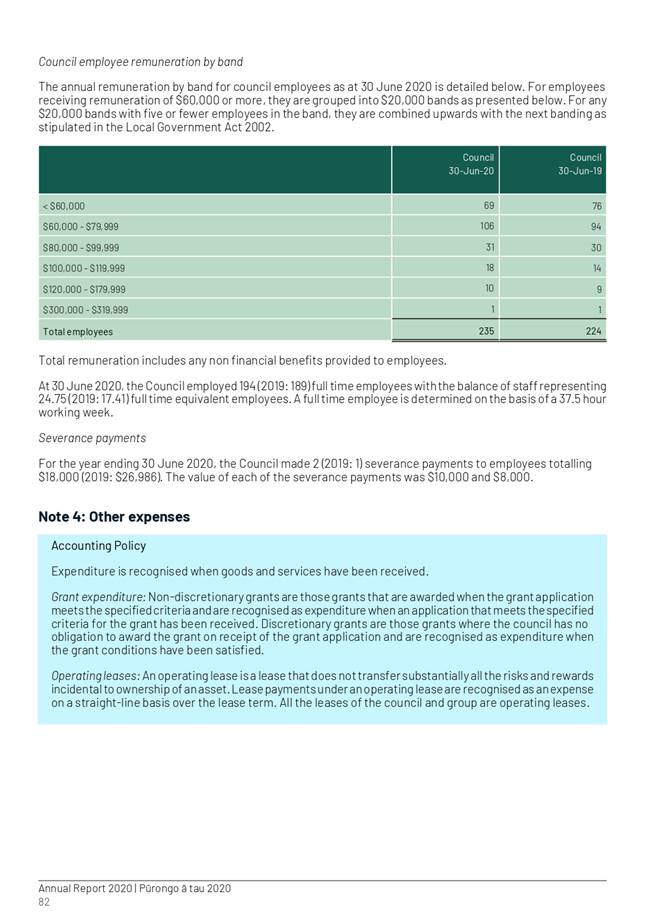

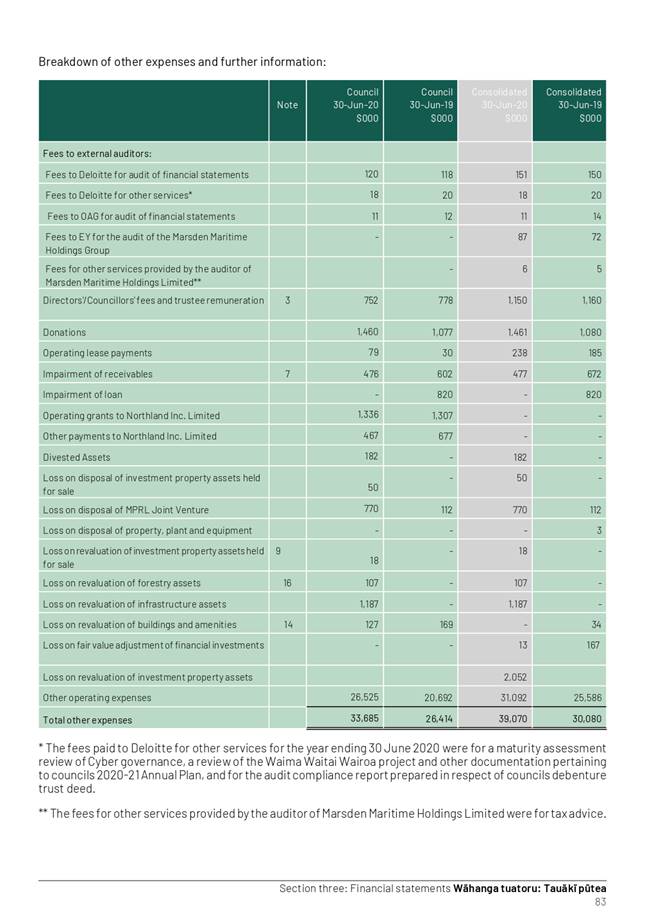

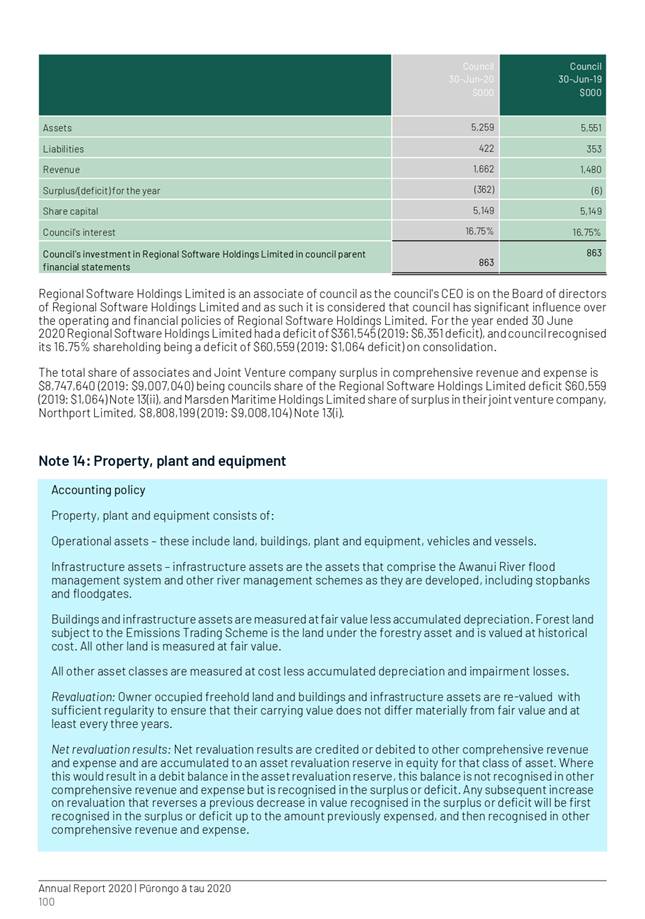

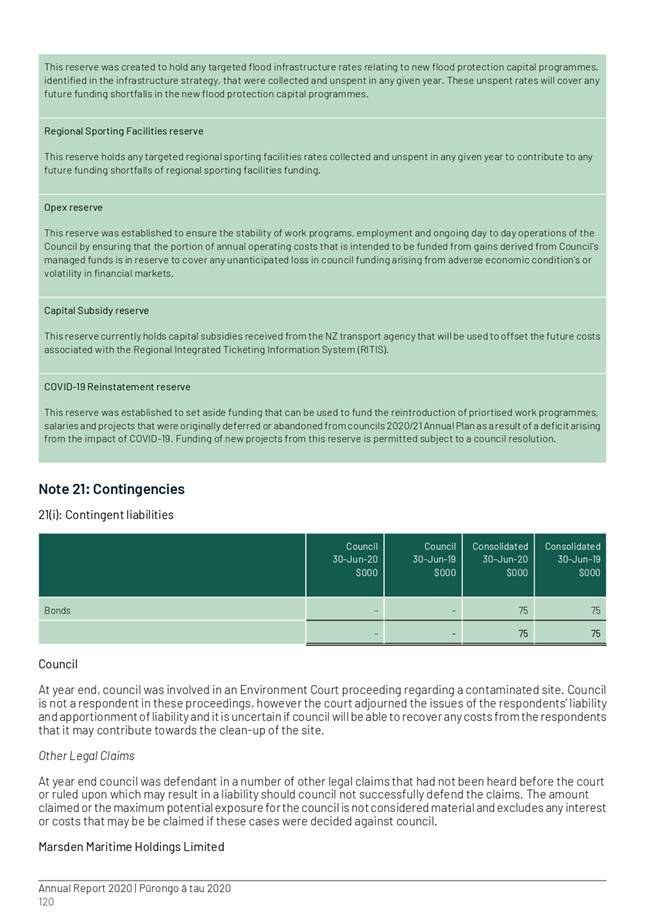

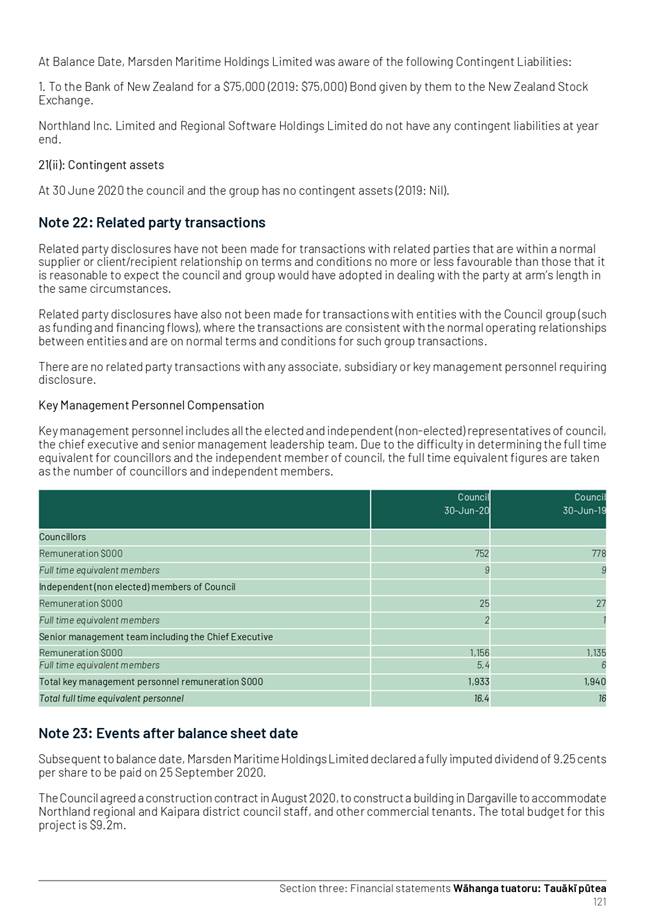

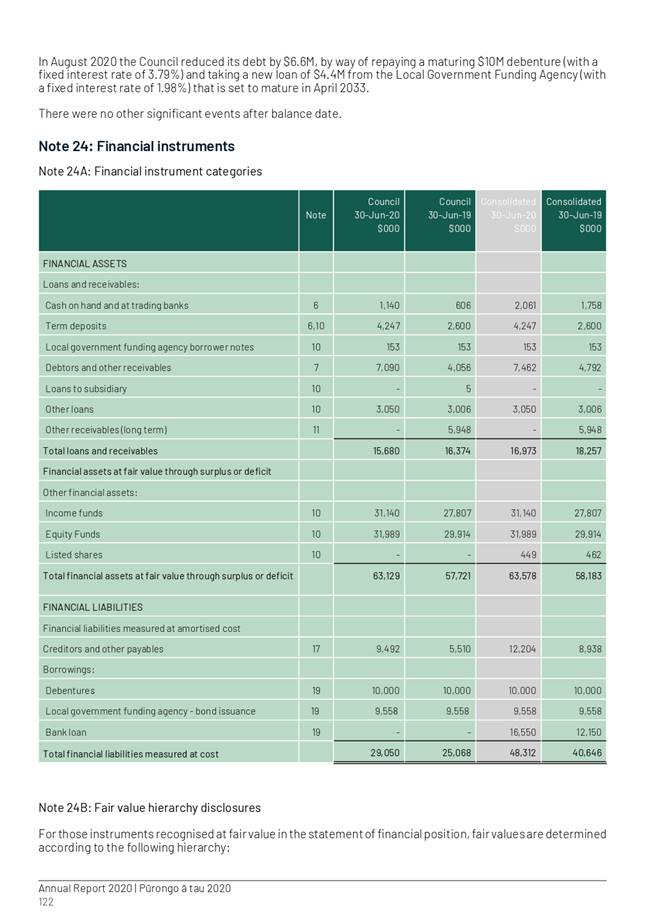

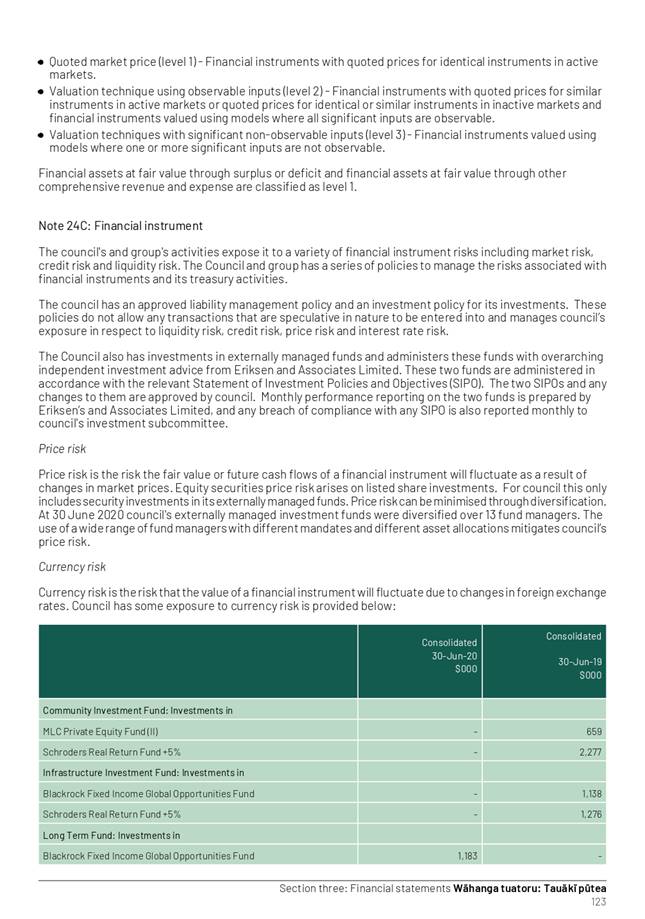

The Deloitte Audit Report on the matters arising from their 2019/20 end of year audit is attached as Attachment One. Peter Gulliver (Deloitte Audit Partner) will attend the September Subcommittee meeting to discuss this report.

The independent member of council, Geoff Copstick, has performed a review of the 2020 Annual Report and has provided a written report summarising his observations, attached as Attachment Two.

The Summary 2020 Annual Report and the Full 2020 Annual Report are attached as Attachment Three and Four respectively. The final formatting and layout of these documents is still being performed.

The final signed audit opinions will be released upon council’s adoption of the Summary and the full Annual Report on 20 October 2020, and Deloitte receiving the signed letters of compliance and representation.

1. That the report ‘2019/20 Annual Report and Deloitte Audit Report’ by Simon Crabb, Finance Manager and dated 10 September 2020, be received.

2. That the Subcommittee endorse a recommendation to council that the Summary Annual Report, the Full Annual Report, and the financial statements for the year ended 30 June 2020 be adopted.

Background/Tuhinga

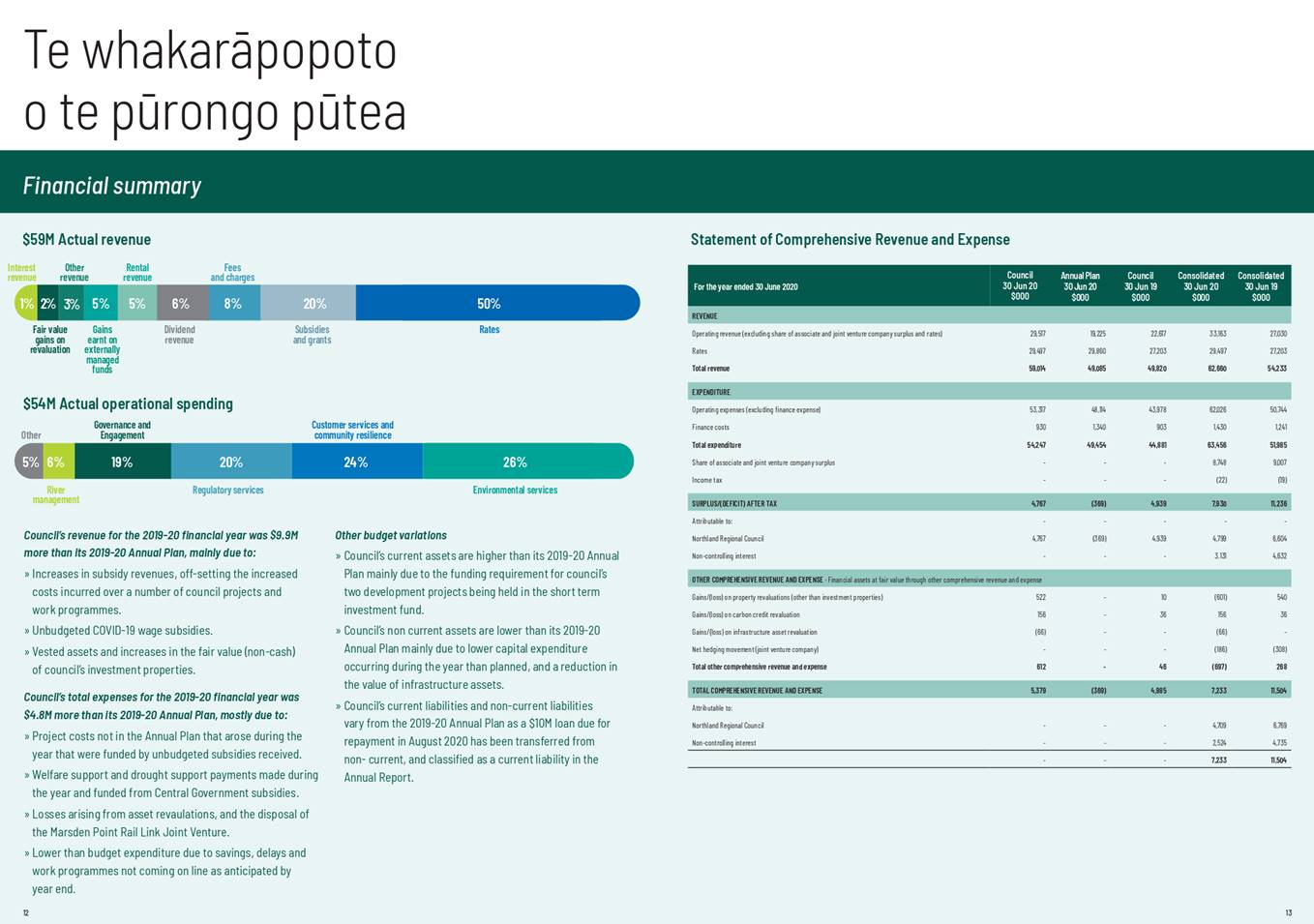

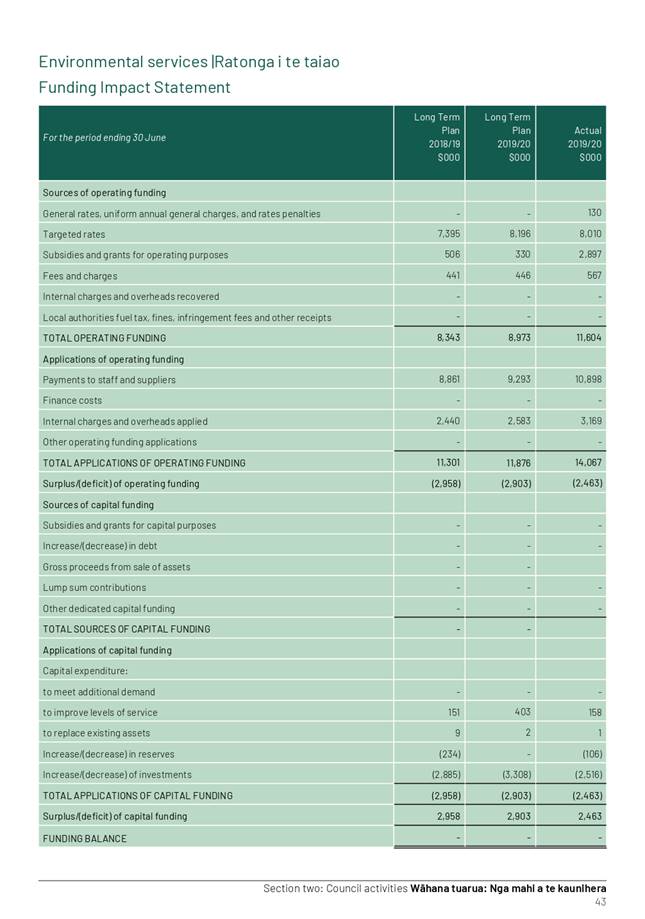

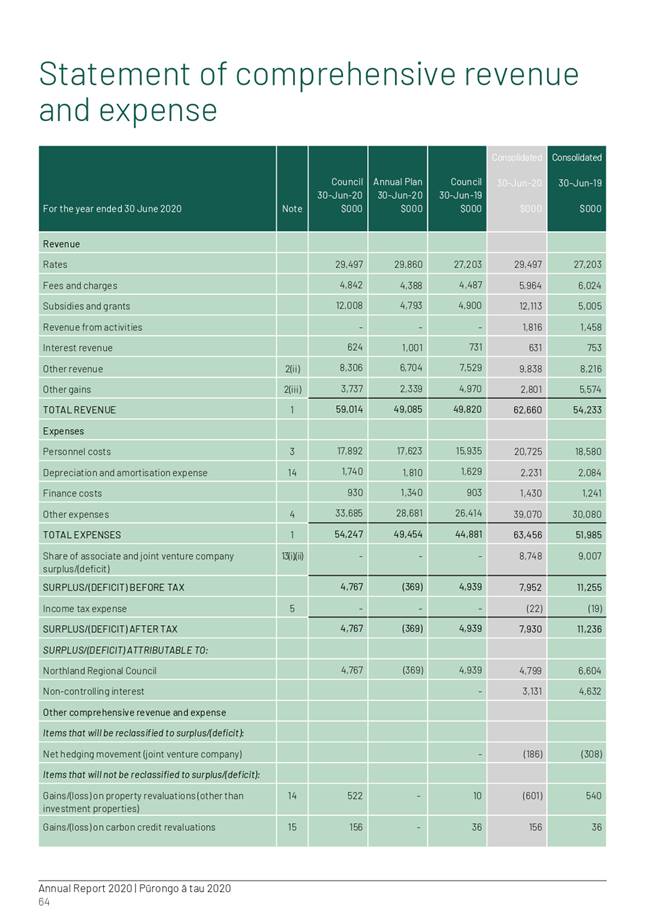

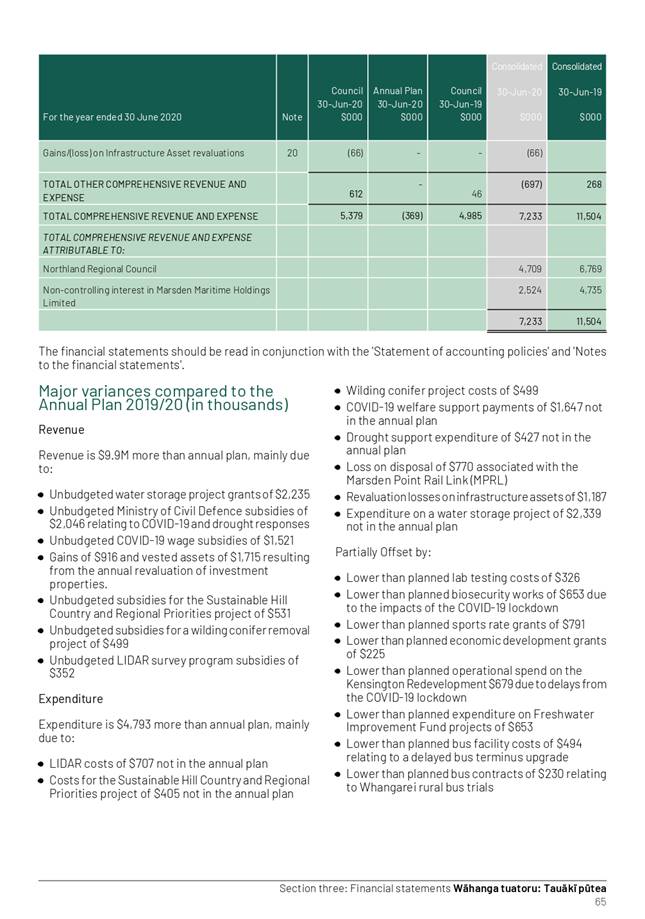

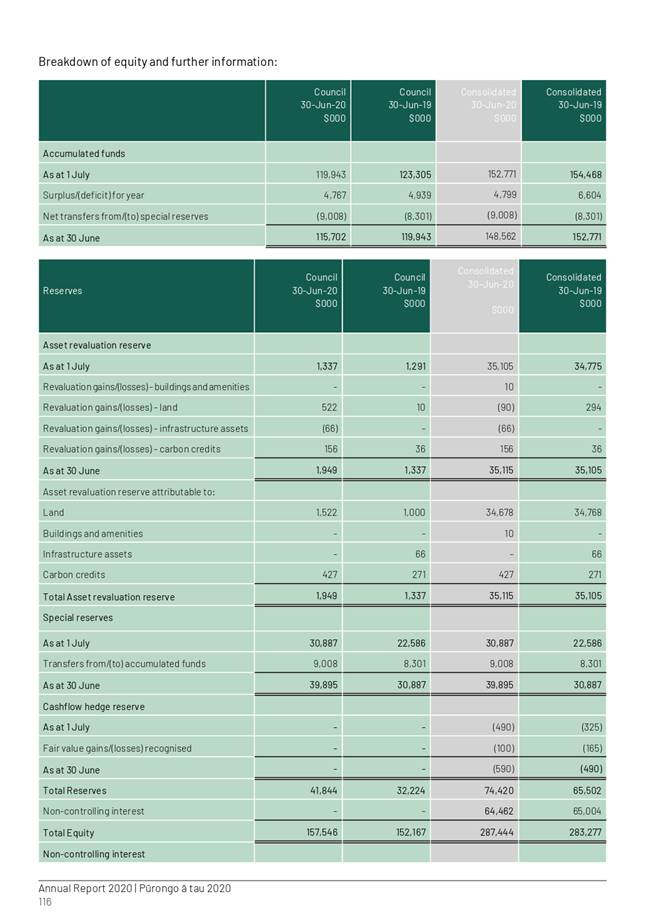

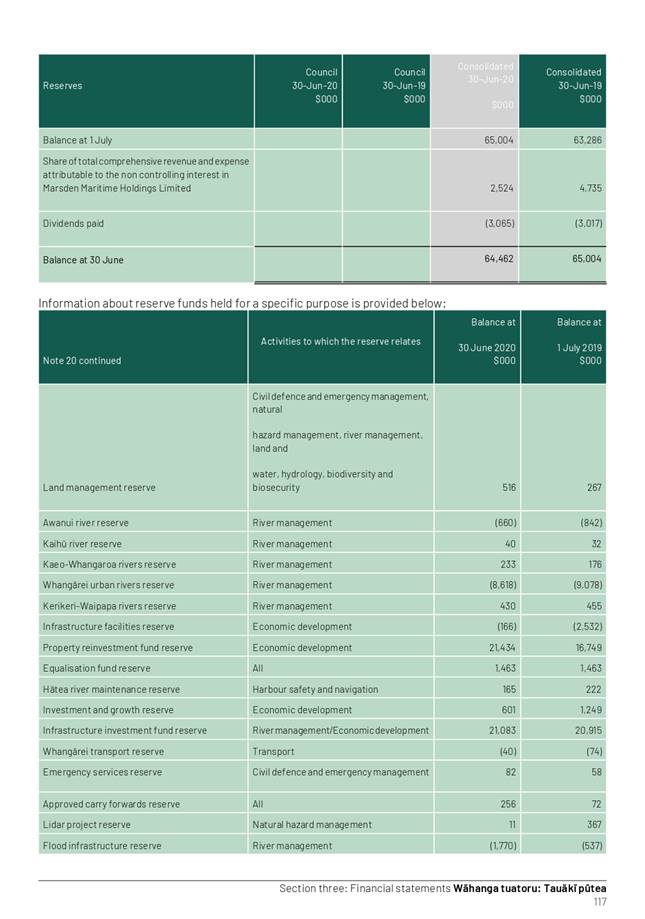

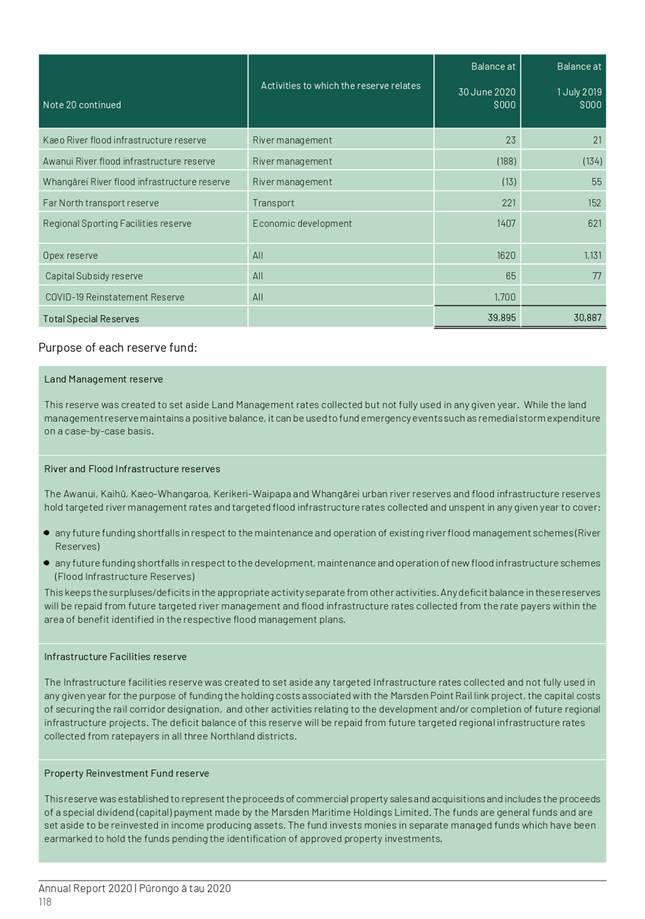

2019-20 Financial Result

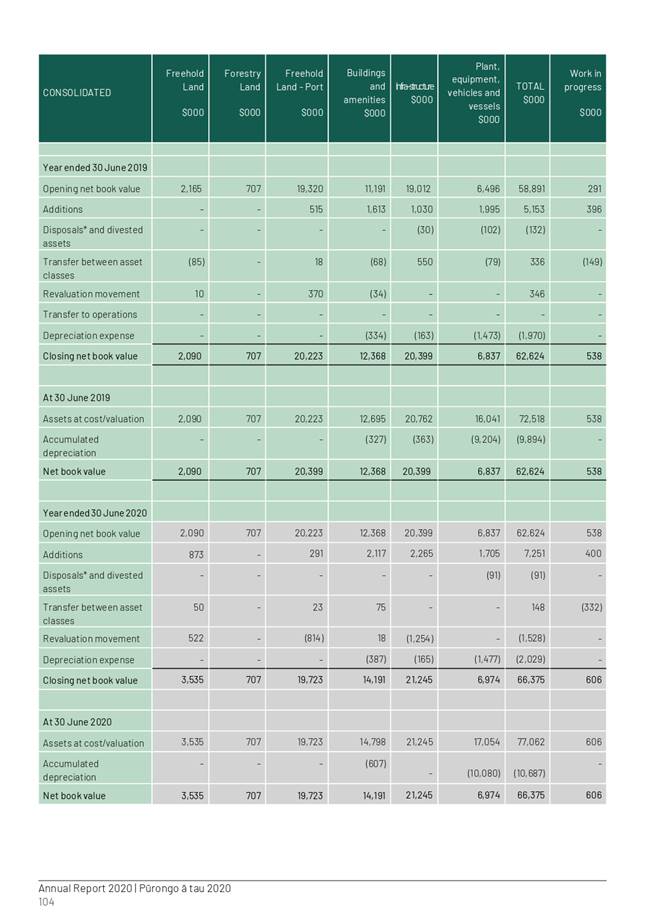

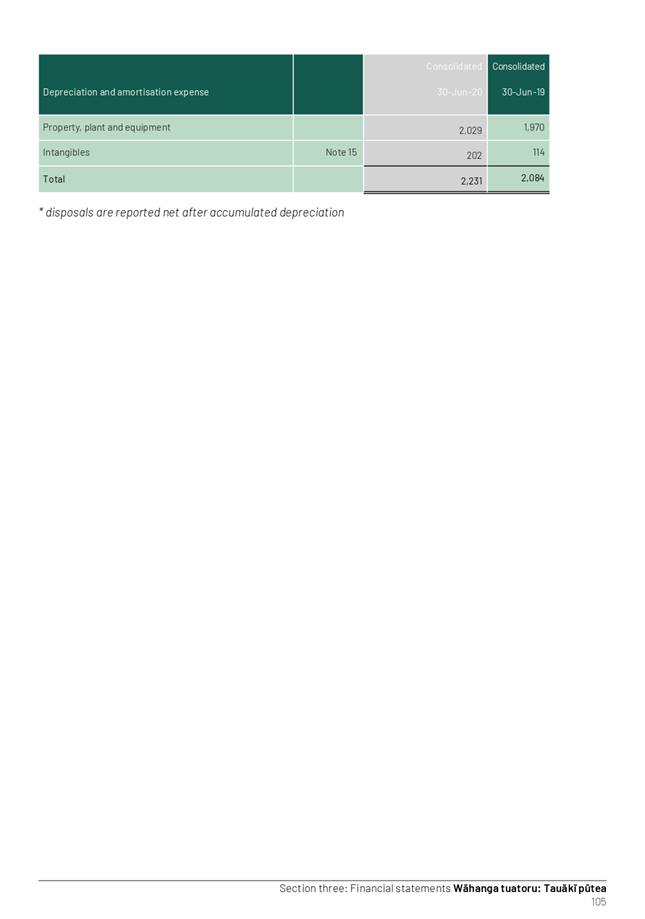

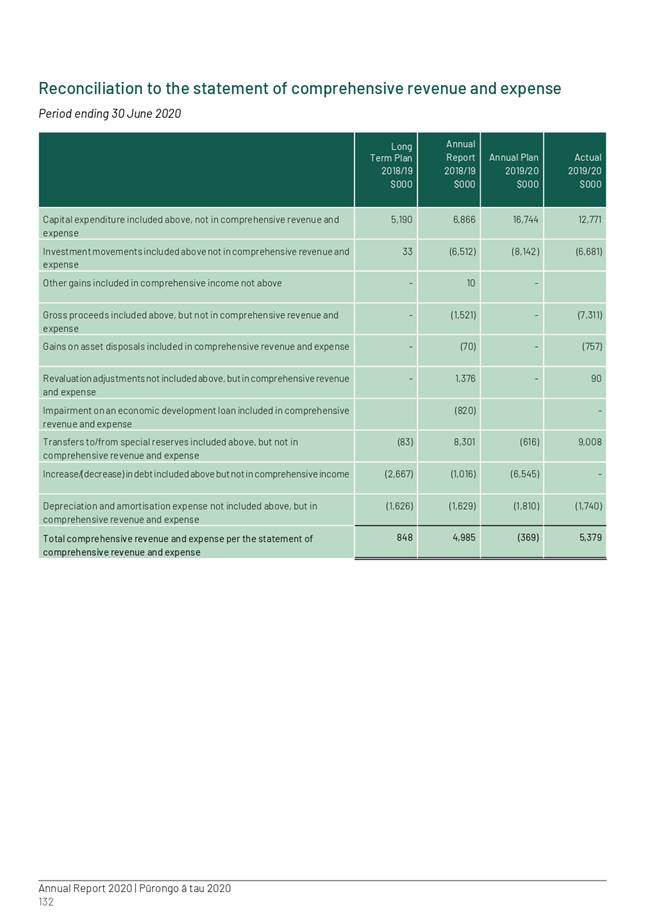

Council posted a total comprehensive revenue and expense surplus for the 2019/20 financial year of $5.38M. At the August 2020 council meeting, the draft net surplus after transfers from/(to) special reserves presented to council was $40K.

The movement from the draft result to the total comprehensive revenue and expense reported in the 2020 Report is explained in Table One over the page.

Table One

|

2019/20 DRAFT net

surplus after transfers to reserves |

40,311 |

|

Add back the transfers to Special Reserves as these do not form part of the statutory reporting format |

2,787,233 |

|

Add back the transfer to reserves approved by Council in August as they do not form part of the statutory reporting format: |

|

|

- COVID-19 Reinstatement Reserve |

1,700,000 |

|

- Opex Reserve |

467,695 |

|

Add back non-cash gains/(losses) on the revaluation of council’s assets: |

|

|

- Investment properties & vested assets |

1,149,349 |

|

- Owner occupied land & buildings |

394,411 |

|

- Carbon credits |

156,267 |

|

- NEST Loan interest |

43,775 |

|

- Infrastructure assets |

(1,253,564) |

|

- Forestry holdings |

(107,000) |

|

Total Comprehensive

Revenue & Expense - |

$5,378,477 |

Deloitte Audit Report

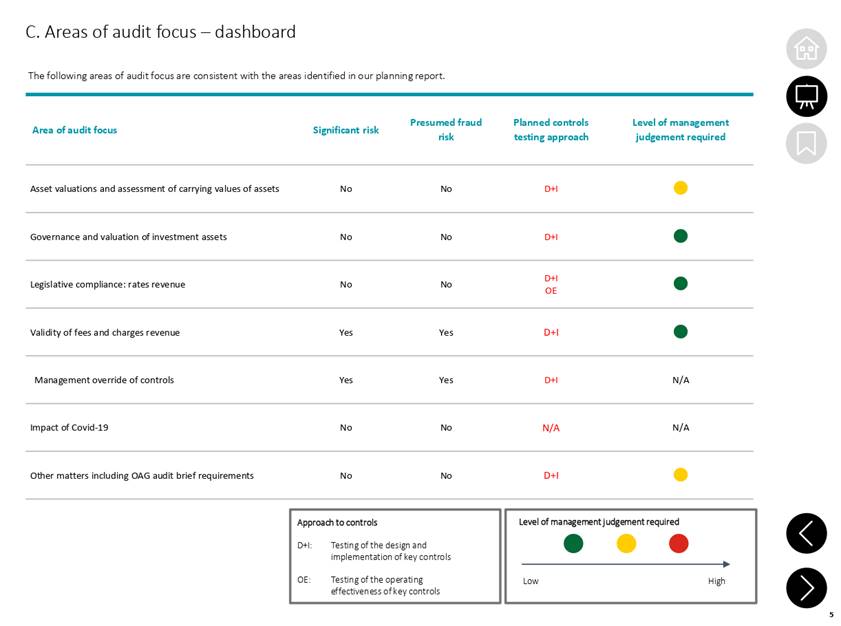

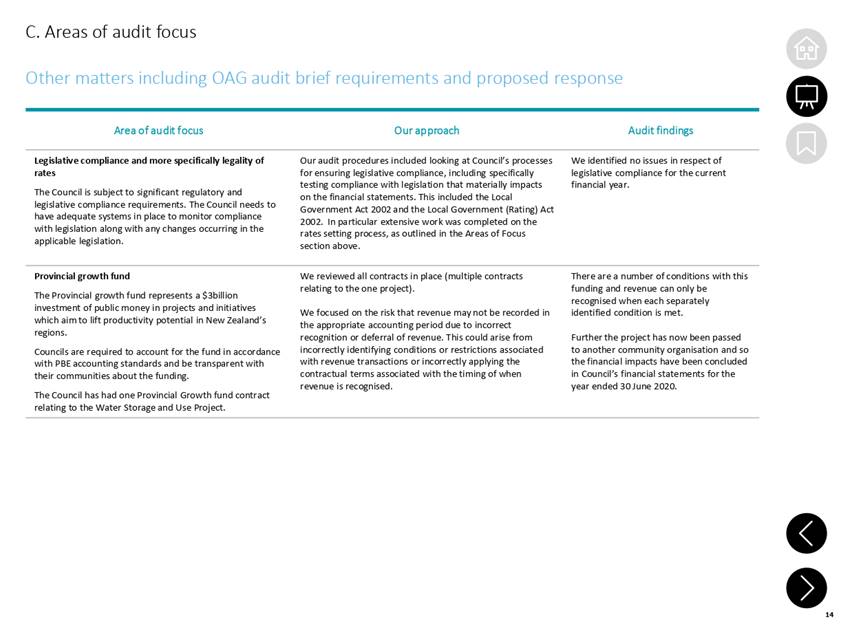

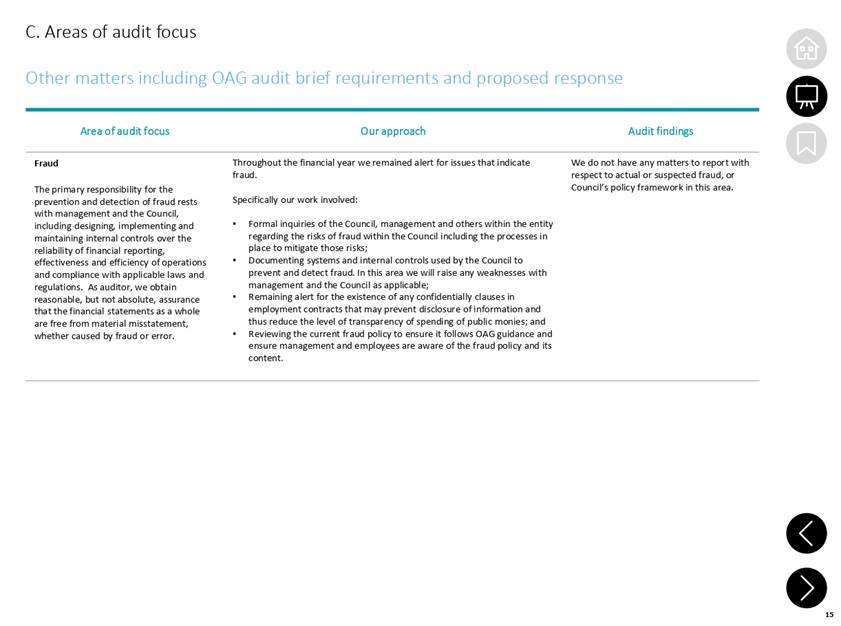

The following two matters were included as part of the Audit findings commentary in the Deloitte Audit report (refer Attachment Three) and will be discussed further by the Audit partner (Peter Gulliver) at the Subcommittee meeting.

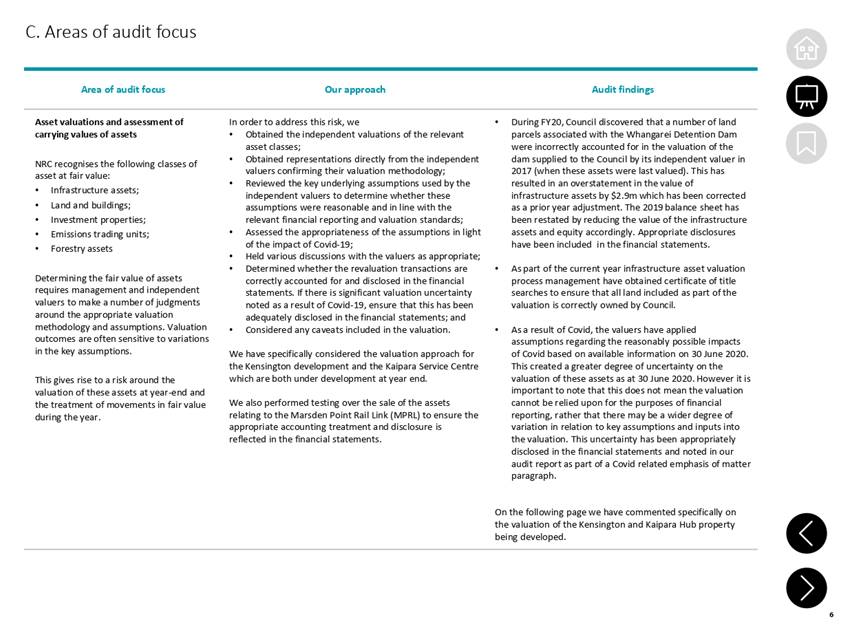

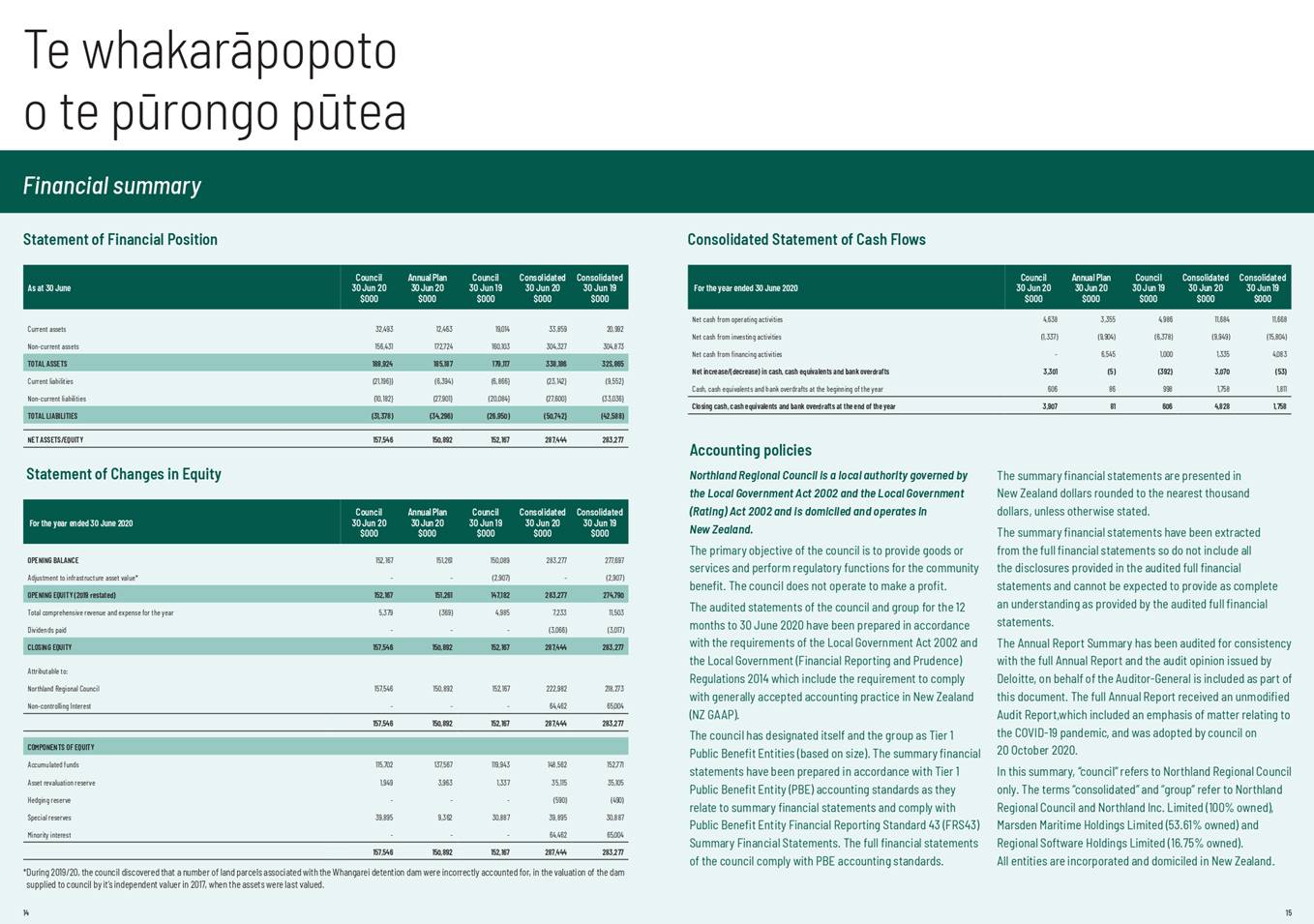

1. Restatement of Prior Year Infrastructure values

During this year’s annual reporting programme it was discovered that several land parcels associated with the Whangarei Detention Dam were incorrectly accounted for in the last valuation (2017) of the dam supplied to NRC by its independent valuer.

Council holds an easement to use a number of land parcels associated with the dam, and in 2017 these parcels were incorrectly valued based on full ownership, while a small amount ($58K) of valid land was excluded from the valuation. The overall impact was a net overstatement in the value of the Dam in 2017 of $2.9M.

This overstatement was corrected in the 2020 financial statements by reducing the opening balance of the Dam assets and council’s equity, by $2.9M in the 2019 financial figures (the comparative column).

To avoid this oversight happening again, a record of title will be required to be held on file by the department responsible for engaging an independent valuer. Furthermore, all valuation reports will be confirmed as correct, with reference to any title records, by the council officer responsible for the asset valuation.

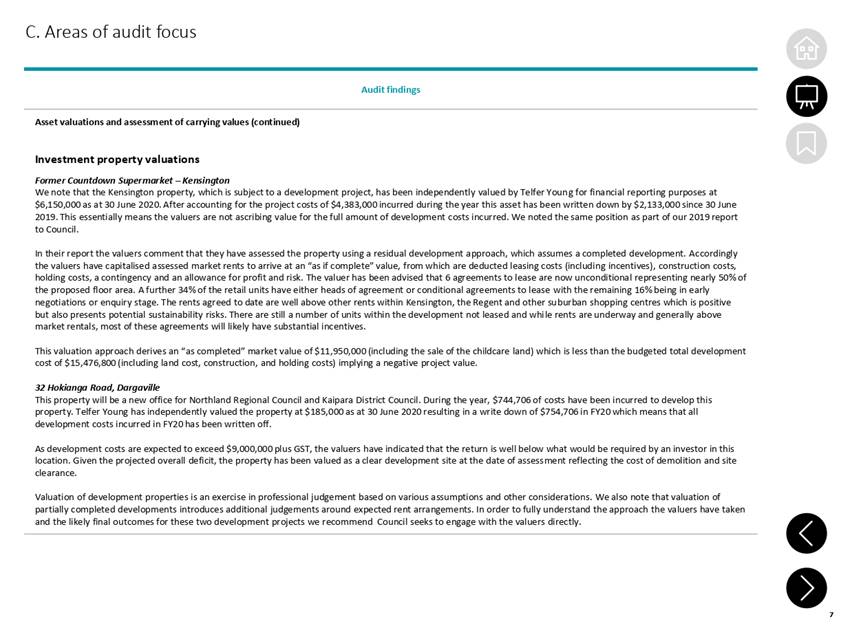

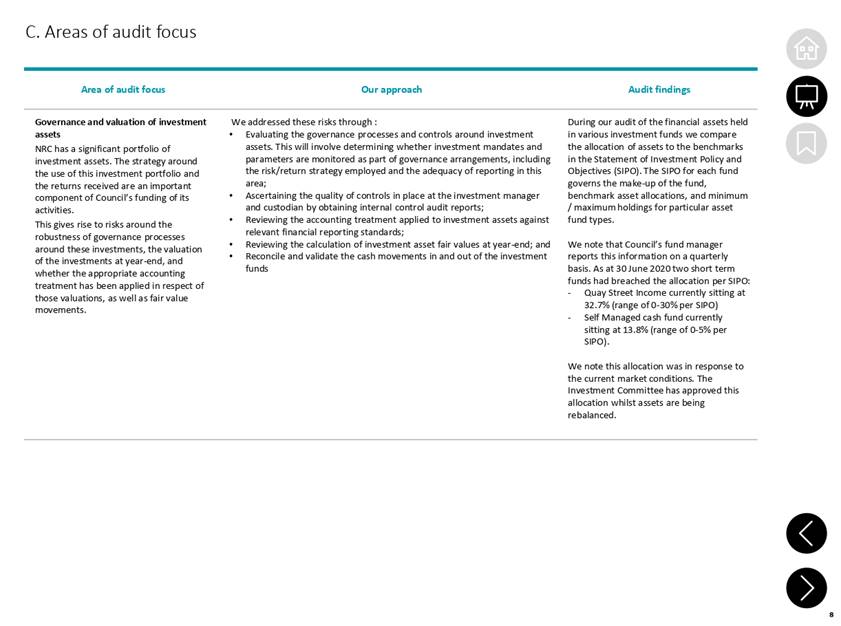

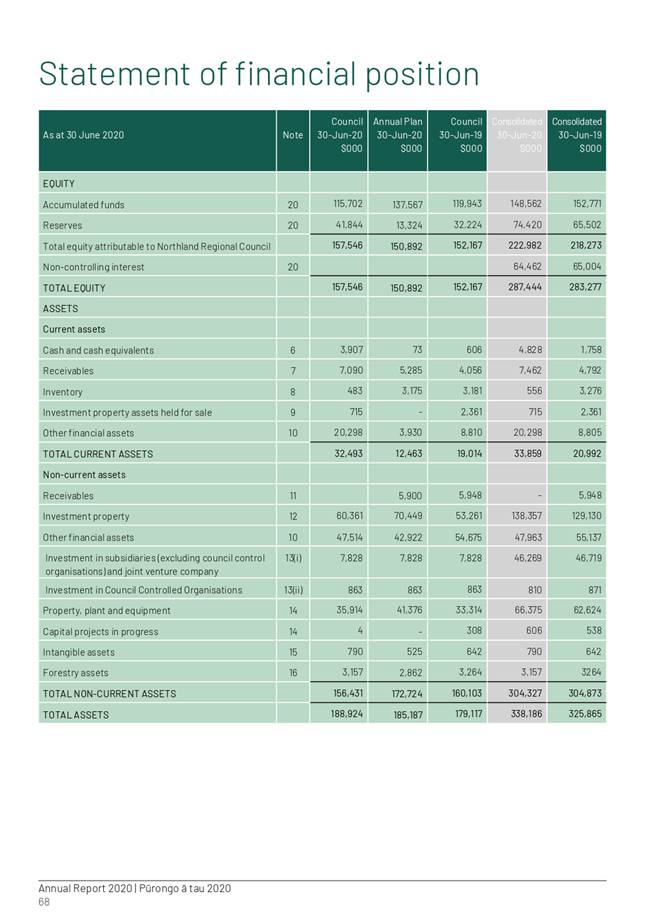

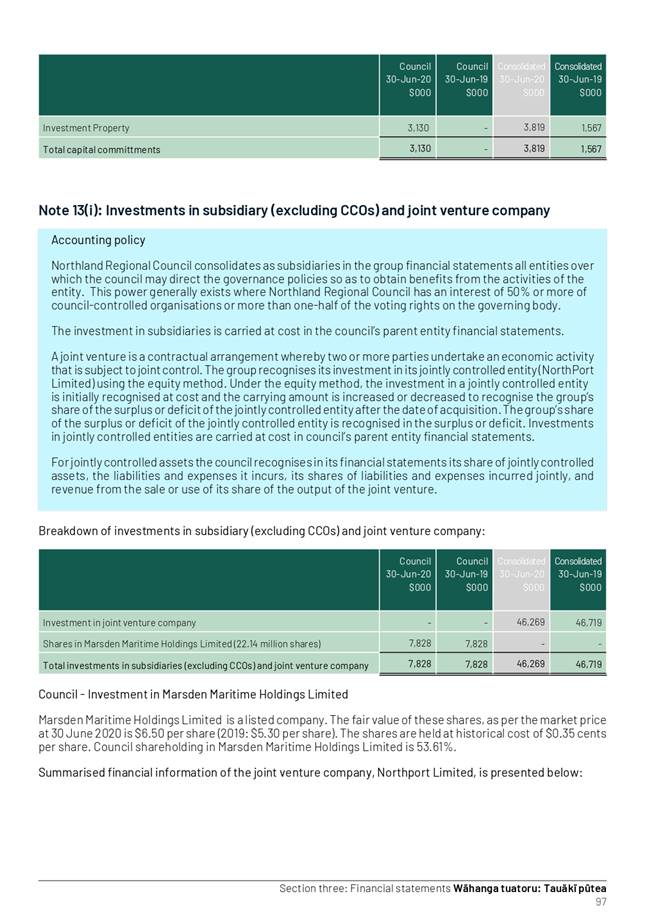

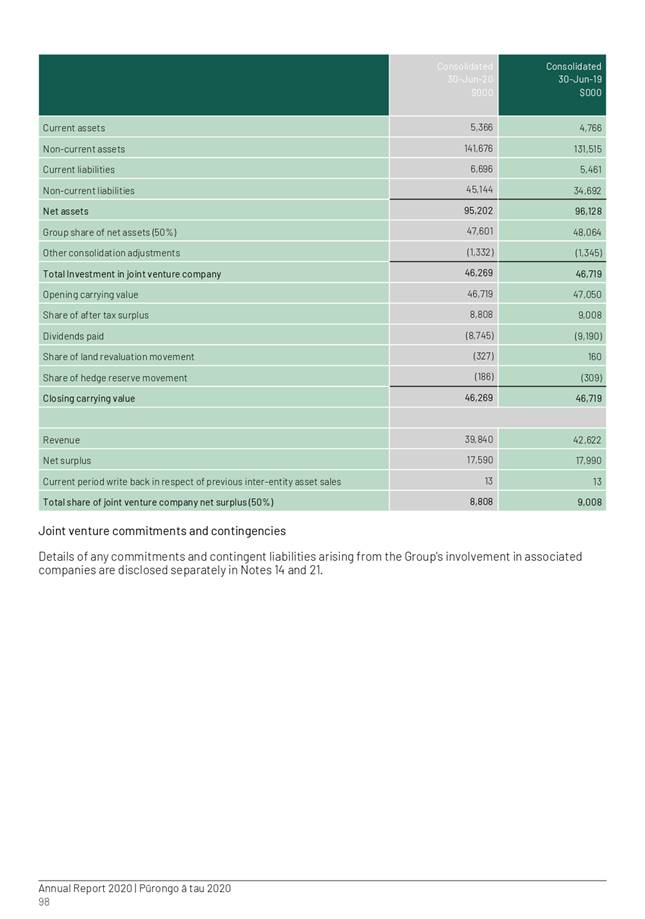

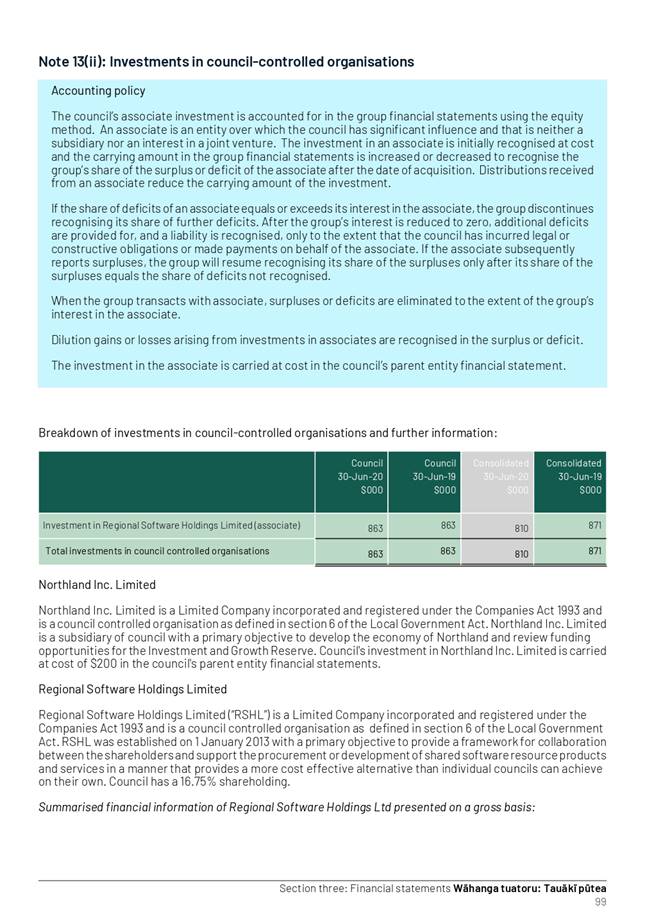

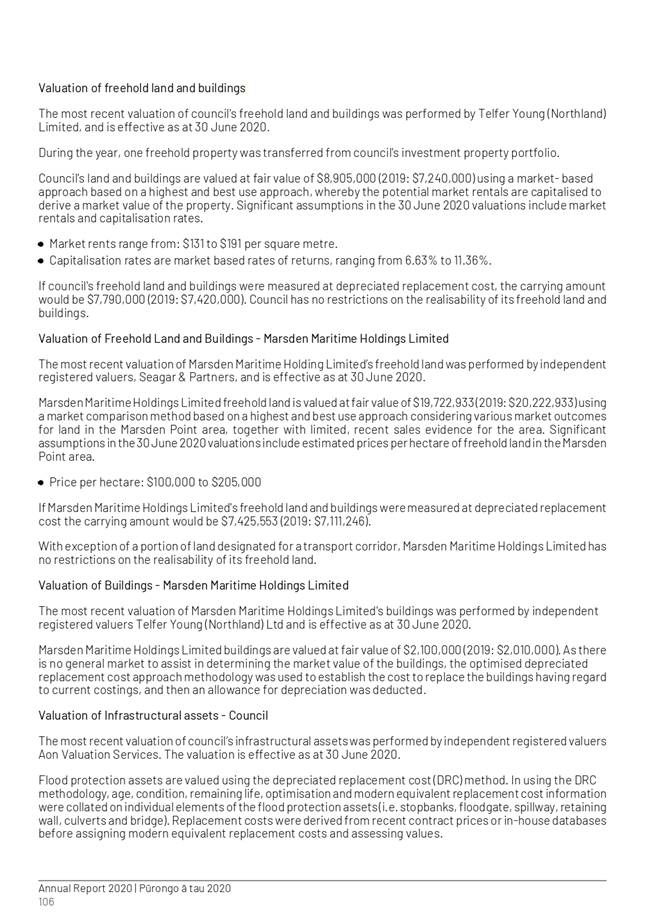

2. Investment Property Valuations

a. Independent Valuation of the Kensington Development Project

In determining the market value of the Kensington Development Project at 30 June 2020, councils independent valuers (Telfer Young) used an approach that calculated a completed development value of $11,950,000 inclusive of the sales proceeds of the childcare site.

The budgeted cost of project is $15,476,800 (including land, construction and holding costs), which implies that in the view of Telfer Young the value of the completed project is going to be less than overall cost of the project.

b. Independent Valuation of the Kaipara Service Centre Development Project

Telfer Young valued the Kaipara Service Centre Development Project at 30 June 2020 at $185K reflecting the costs of demolition and site clearance only, disregarding the development costs spent to date of approximately $745K.

Telfer Young also stated in their valuation report that the return from investment of the Kaipara Service Centre project “is well below what would be required by an investor in this location”.

In reference to 2a and 2b, Deloitte make the point that property valuations are based on a number of assumptions and professional judgement. Deloitte suggest council may want to consider engaging with Telfer Young directly to fully understand their assumptions and the approach that underpins the values attributed to these two development projects.

Considerations

1. Options

|

No. |

Option |

Advantages |

Disadvantages |

|

1 |

Adopt |

Facilitate the adoption and public availability of the 2020 Annual Report and 2020 Summary Annual Report within the statutory timeframes set out in the LGA 2002. |

None |

|

2 |

Do not Adopt |

The annual report can be amended if required |

A special council meeting would need to be called before 31 October 20 to adopt a revised 2020 Annual Report and comply with the Local Electoral Act 2001 and the Local Government Act 2002. |

The staff’s recommended option is 1.

2. Significance and engagement

In relation to section 79 of the Local Government Act 2002, this decision is considered to be of low significance when assessed against council’s Significance and Engagement Policy because it has previously been consulted on and provided for in council’s Long Term Plan and/or is part of council’s day to day activities. This does not mean that this matter is not of significance to tāngata whenua and/or individual communities, but that council is able to make decisions relating to this matter without undertaking further consultation or engagement.

3. Policy, risk management and legislative compliance

Endorsement of the recommendations is consistent with sections 98 and 99 of the Local Government Act 2002 regarding the timeframes for adoption and public availability of the annual report and the requirement for an audit report to be included in both the full Annual Report and Summary Annual Report.

Further considerations

Being a purely administrative matter, financial implications, community views, and Māori impact statement are not applicable.

Attachments/Ngā tapirihanga

Attachment 1: 2019/20 Deloitte Audit

Report ⇩ ![]()

Attachment 2: 2019/20 Geoff Copstick

Commentary ⇩ ![]()

Attachment 3: 2019/20 Annual Report

Summary ⇩ ![]()

Attachment 4: 2019/20 Annual Report ⇩ ![]()

Authorised by Group Manager

|

Name: |

Bruce Howse, Group Manager - Corporate Excellence, |

|

Title: |

Group Manager - Corporate Excellence |

|

Date: |

|

6 October 2020

|

TITLE: |

Risk Management Activity- Update |

|

ID: |

A1356751 |

|

From: |

Kym Ace, Corporate Systems Champion |

Executive summary/Whakarāpopototanga

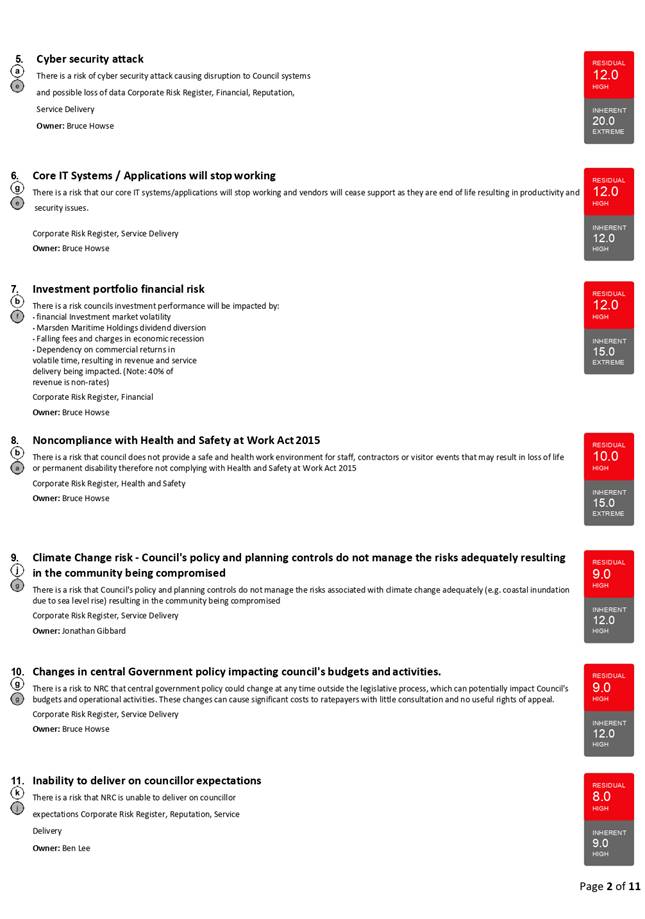

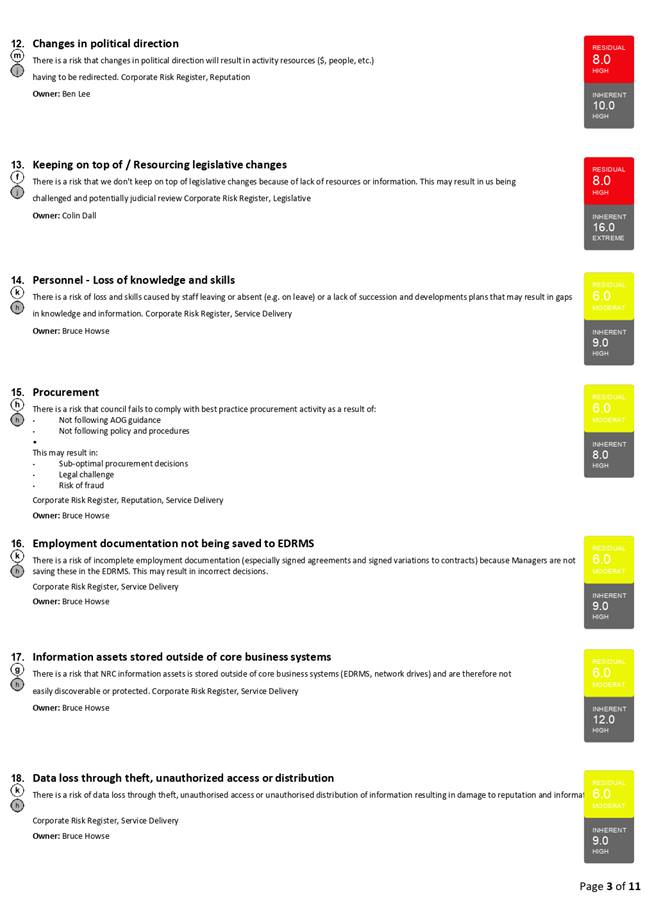

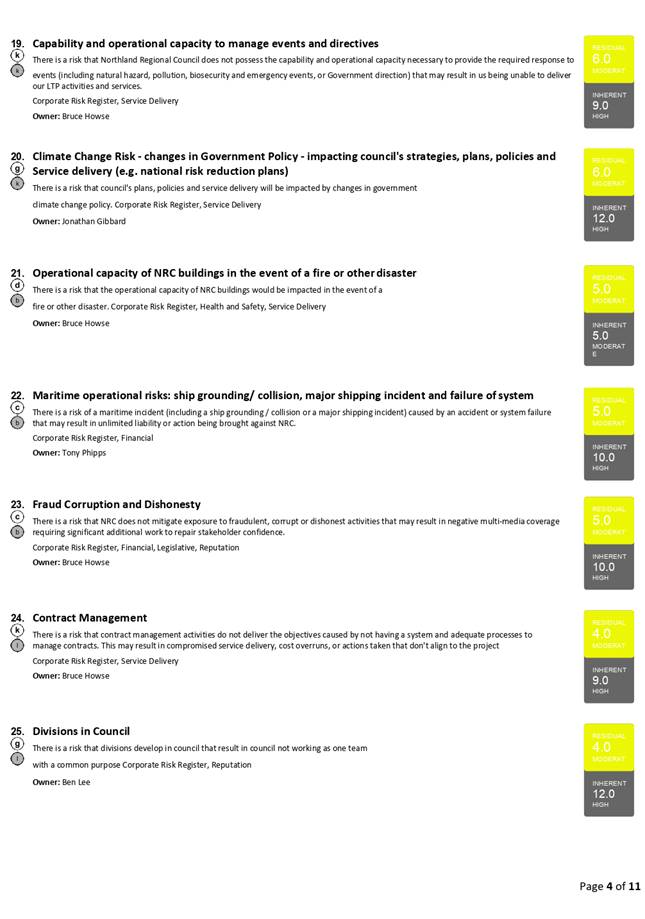

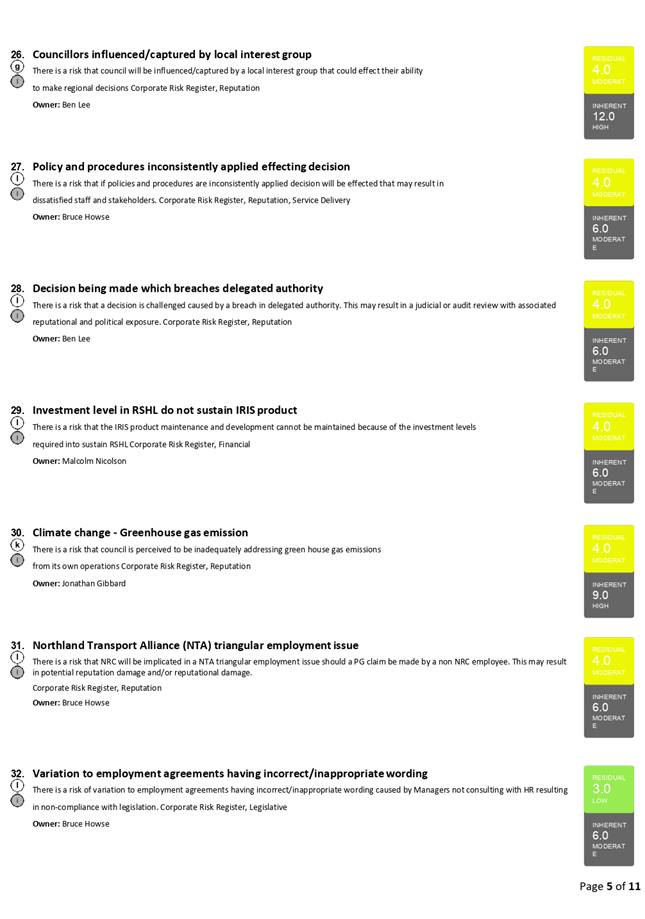

The Risk Management Activity Update Report outlines the summary of Council’s progress in risk

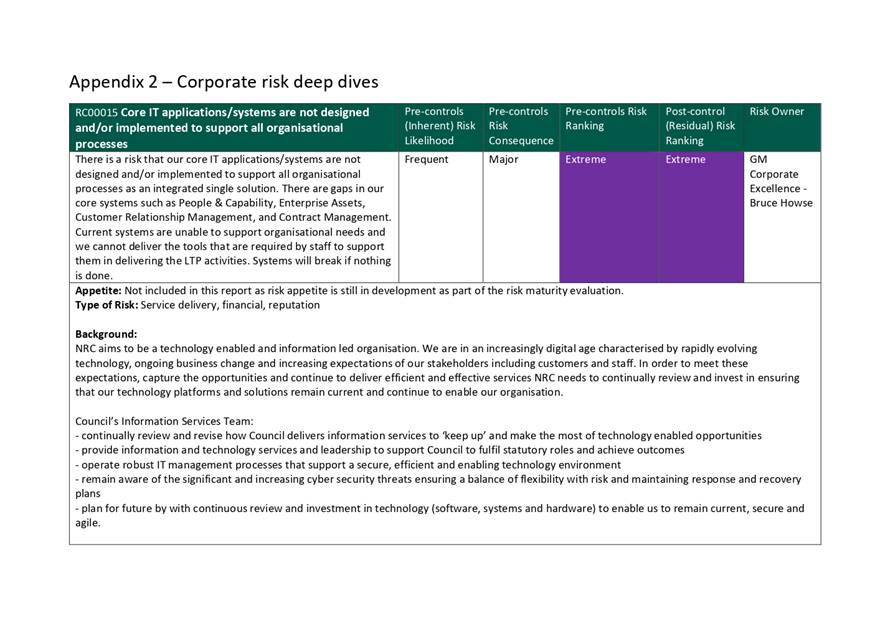

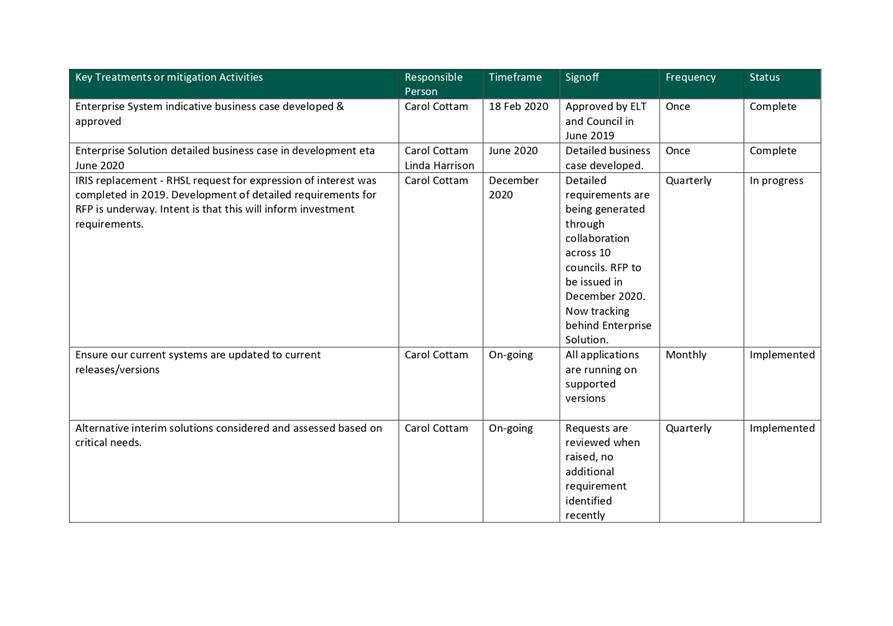

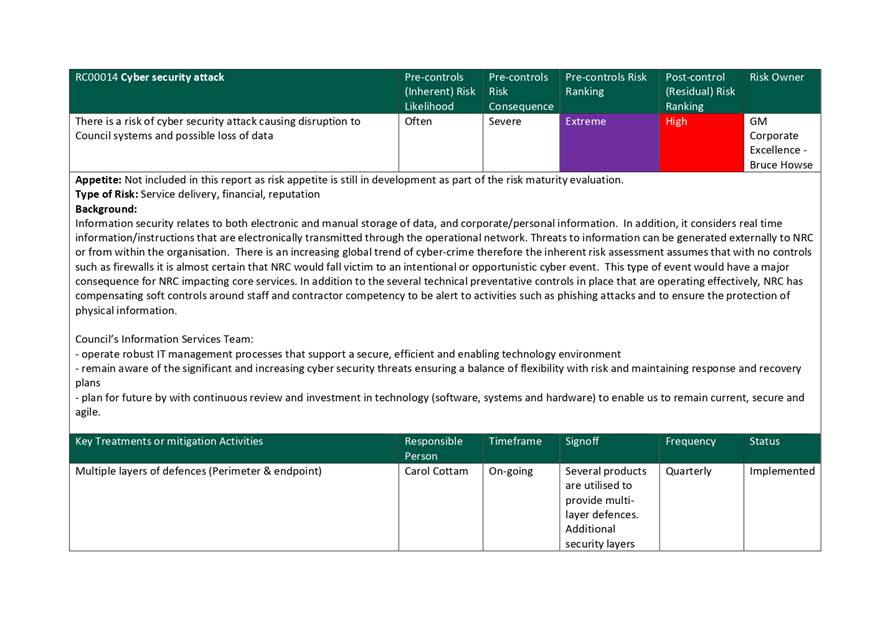

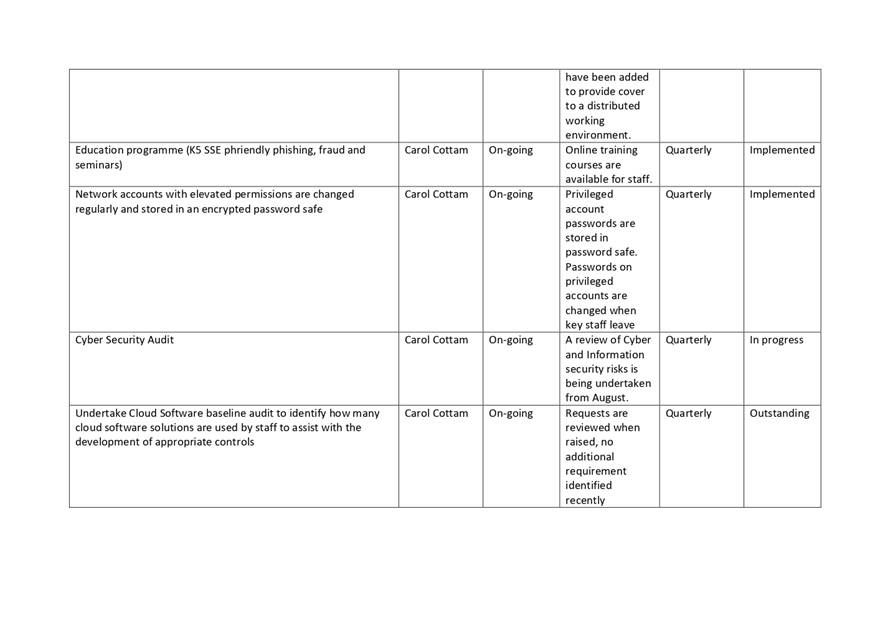

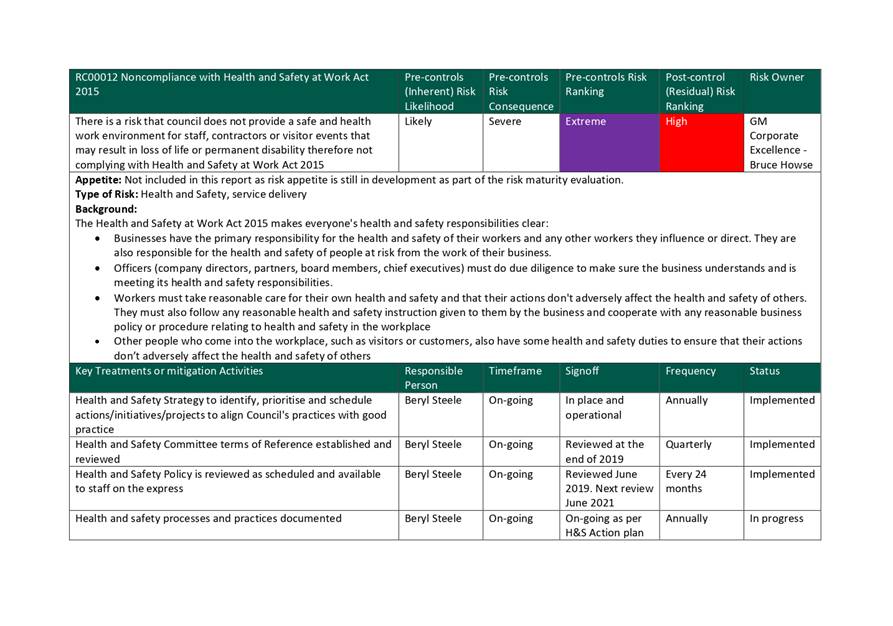

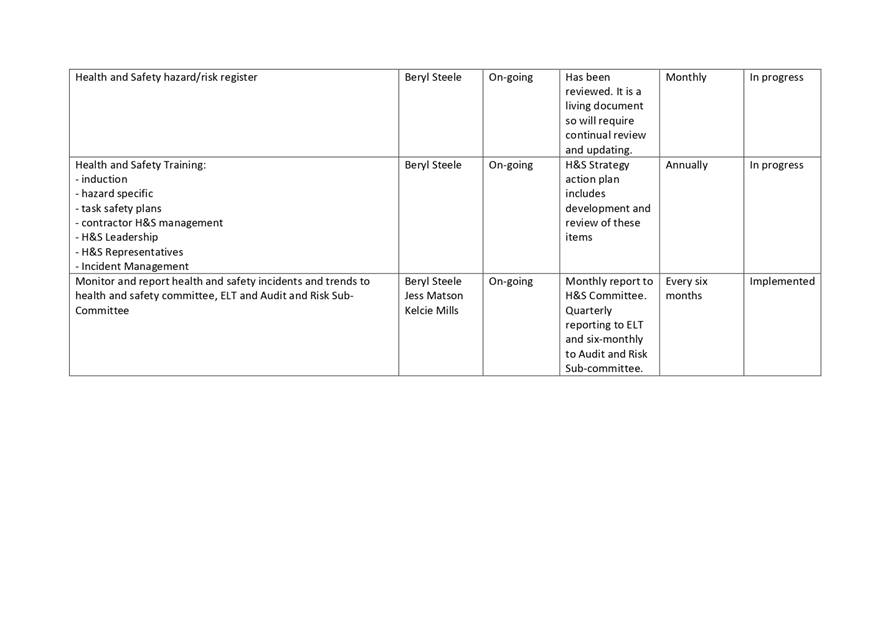

management related activities including updates on Corporate and Group Risks and deep dives into Corporate Risk RC00015 Core IT applications/systems, RC00014 Cyber security attack and RC00012 Noncompliance with Health and Safety at Work Act.

That the report ‘Risk Management Activity- Update ’ by Kym Ace, Corporate Systems Champion and dated 26 August 2020, be received.

Background/Tuhinga

Risks Register

1. The corporate and group risk registers have now been migrated from the excel spreadsheets into the Promapp risk module.

2. The risks and their treatment/s (mitigation action/s) are being managed by staff through the Promapp risk module. Risk reporting will be provided quarterly to the Audit and Risk Subcommittee. The monitoring of the corporate and group risk registers will be performed by the Corporate Systems Champion on a monthly basis.

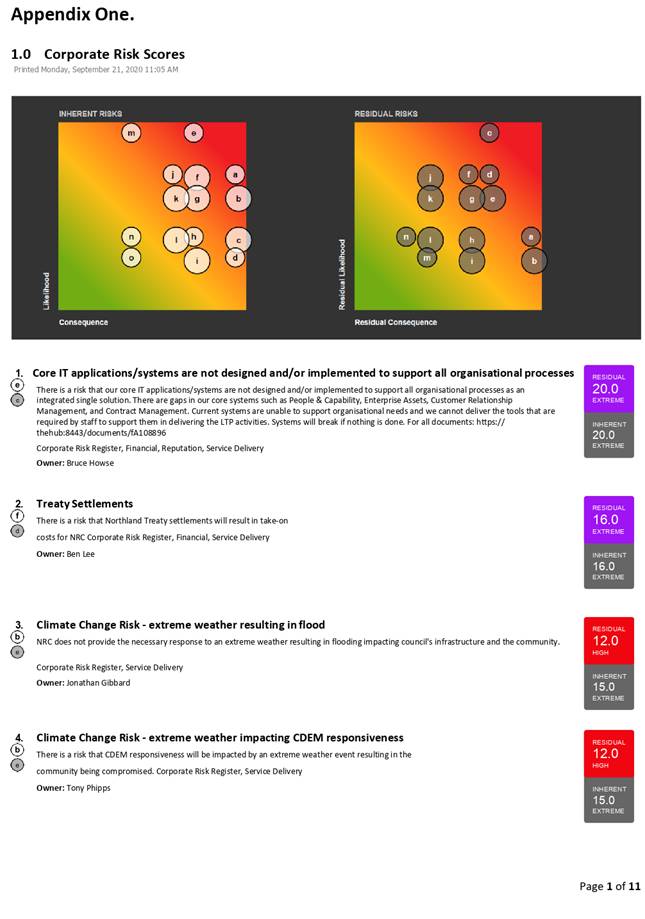

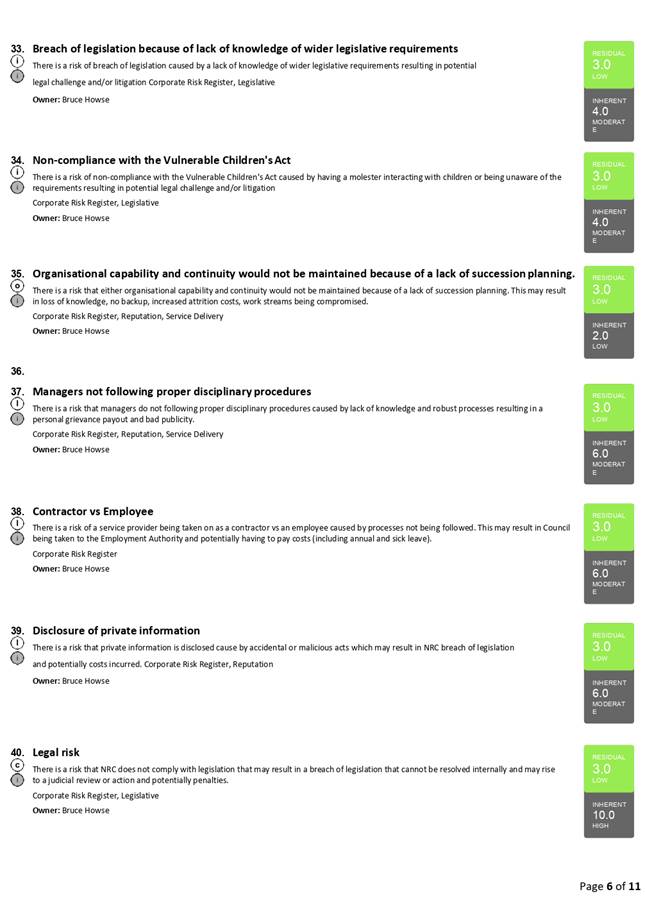

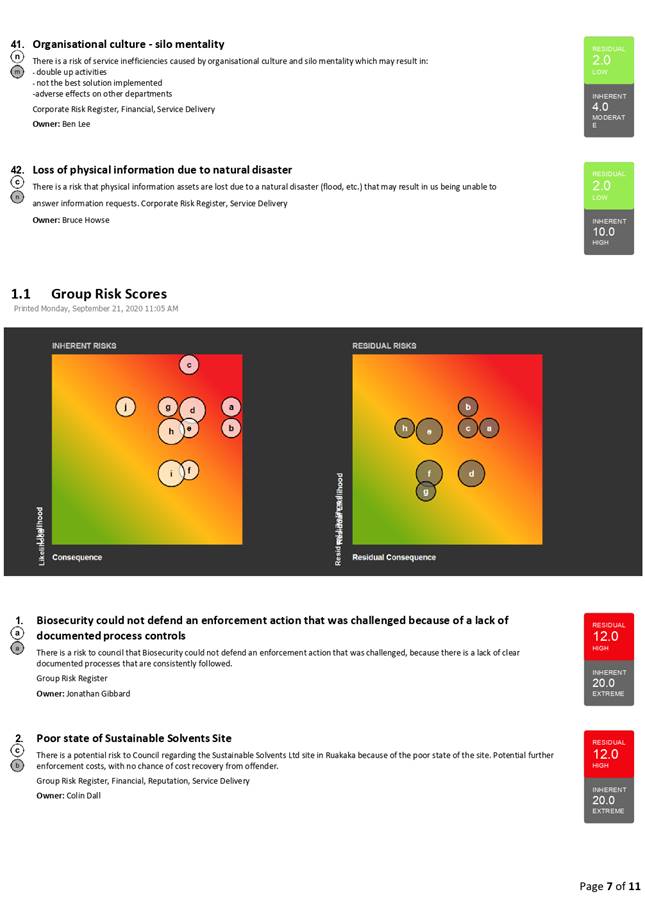

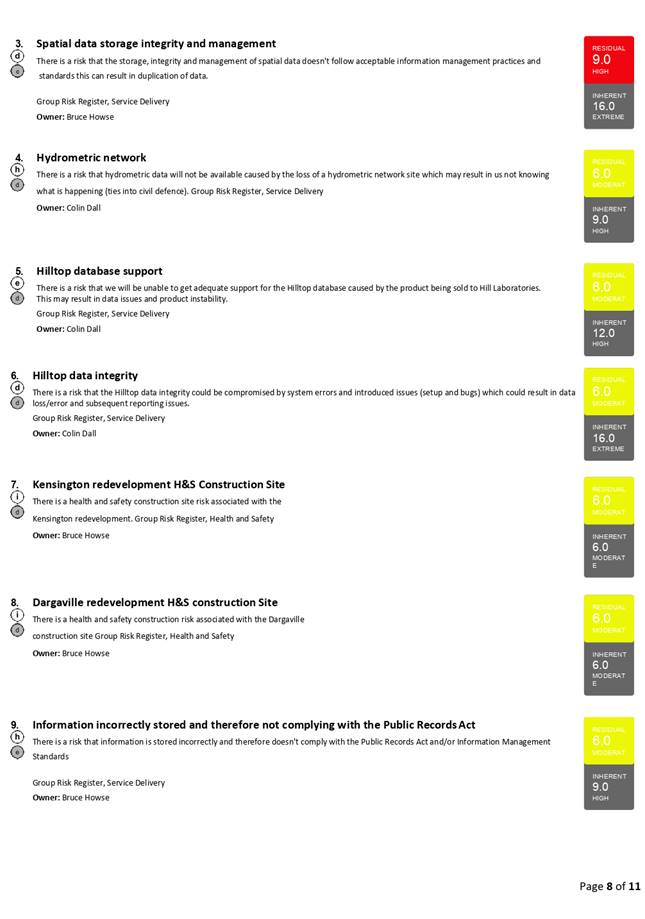

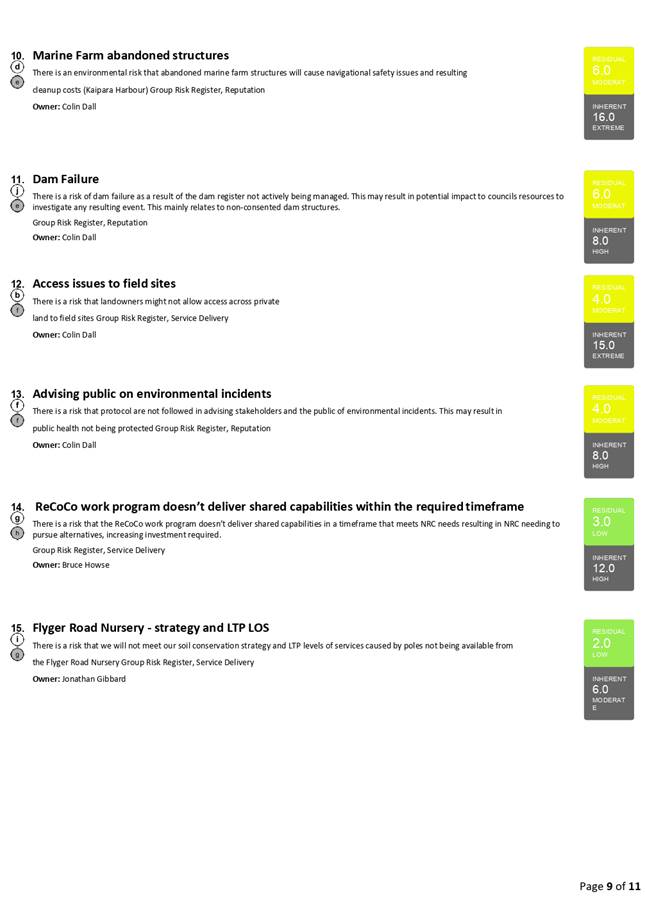

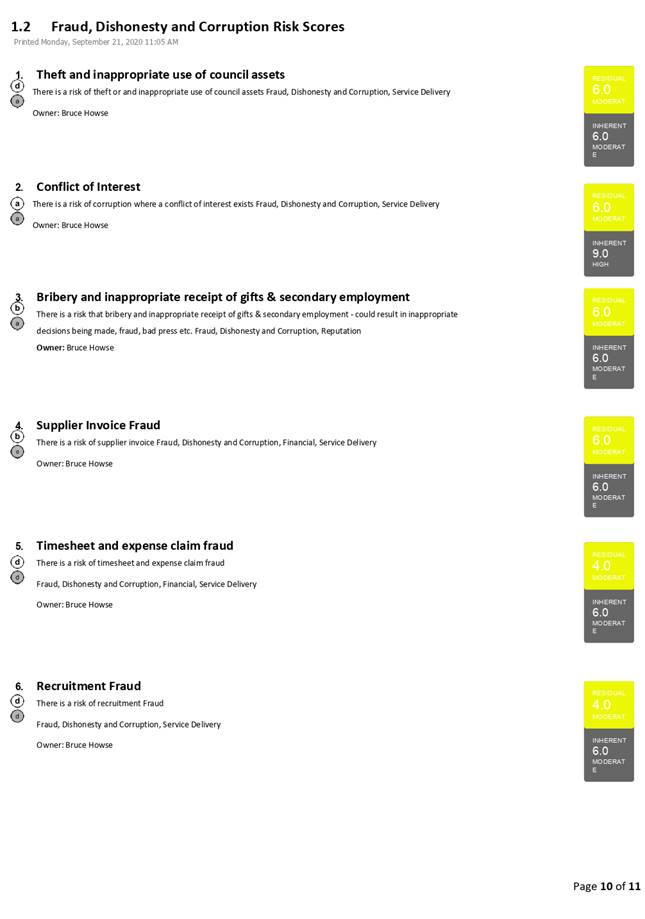

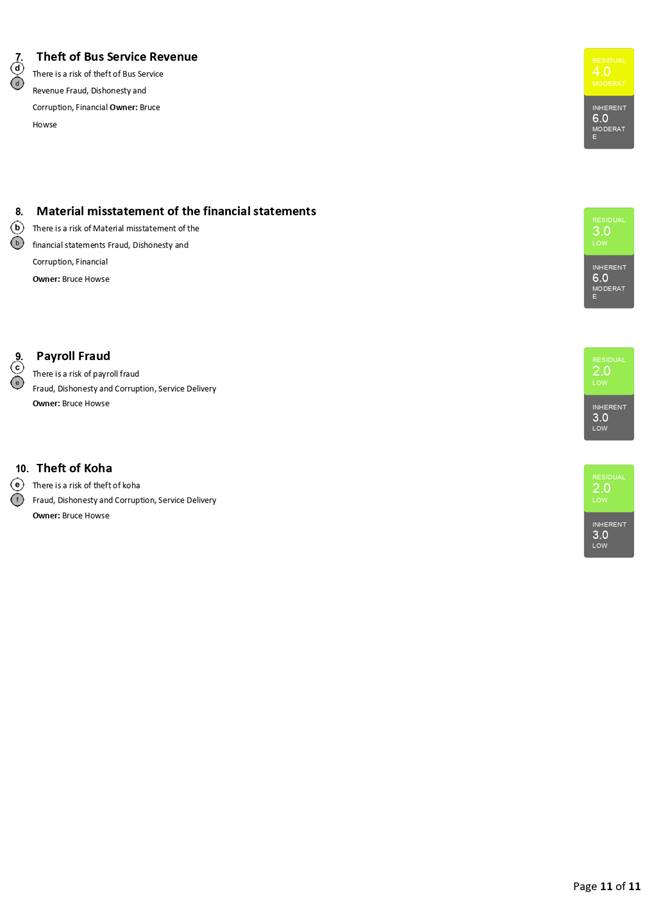

3. The corporate and group risks, their risk types, pre-control (inherent) and post control (residual rating) are summarised in Appendix 1.

Deep Dives

4. The Corporate System Champion facilitates risk owners to provide deep dives into each corporate and or group risk in accordance with the following schedule (Table 1), initially focussing on the corporate risk with the highest pre-controls risk rating e.g. Health and safety, core IT applications/systems and cyber security refer Appendix 2. The number of risks that would require deep dives will depend on the risk appetite set in the framework i.e. all risk that exceed council’s post-control moderate risk appetite for implemented controls.

Table One

|

# |

Corporate Risk |

Sept 2020 |

Dec 2020 |

March 2020 |

|

1 |

Core IT applications/systems |

√ |

|

|

|

2 |

Climate change |

|

√ |

|

|

3 |

Treaty Settlements |

|

|

√ |

|

4 |

Investment Portfolio financial risk |

|

√ |

|

|

5 |

Non-Compliance with Health and Safety at Work Act 2015 |

√ |

|

|

|

6 |

Poor State of Sustainable Solvents Site |

|

|

√ |

|

7 |

Changes in central government policy impacting council’s budgets and activities |

|

√ |

|

|

8 |

Cyber Security attack |

√ |

|

|

|

9 |

Changes in political direction |

|

|

√ |

|

10 |

Inability to deliver on councillor expectations |

|

√ |

|

Attachments/Ngā tapirihanga

Attachment 1: Corporate and Group Risk ⇩ ![]()

Attachment 2: Corporate Risk Deep Dives

⇩ ![]()

Authorised by Group Manager

|

Name: |

Bruce Howse, Group Manager - Corporate Excellence, |

|

Title: |

Group Manager - Corporate Excellence |

|

Date: |

|

Audit and Risk Subcommittee ITEM: 6.0

6 October 2020

|

TITLE: |

Executive Summary

The purpose of this report is to recommend that the public be excluded from the proceedings of this meeting to consider the confidential matters detailed below for the reasons given.

1. That the public be excluded from the proceedings of this meeting to consider confidential matters.

2. That the general subject of the matters to be considered whilst the public is excluded, the reasons for passing this resolution in relation to this matter, and the specific grounds under the Local Government Official Information and Meetings Act 1987 for the passing of this resolution, are as follows:

|

Item No. |

Item Issue |

Reasons/Grounds |

|

6.1 |

Confirmation of Confidential Minutes - 24 June 2020 |

The public conduct of the proceedings would be likely to result in disclosure of information, as stated in the open section of the meeting -. |

|

6.2 |

Up date form AON Insurance |

The public conduct of the proceedings would be likely to result in disclosure of information, the withholding of which is necessary to protect information where the making available of the information would be likely unreasonably to prejudice the commercial position of the person who supplied or who is the subject of the information s7(2)(b)(ii) and the withholding of which is necessary to enable council to carry out, without prejudice or disadvantage, commercial activities s7(2)(h). |

3. That the Independent Financial Advisor be permitted to stay during business with the public excluded.

Considerations

1. Options

Not applicable. This is an administrative procedure.

2. Significance and Engagement

This is a procedural matter required by law. Hence when assessed against council policy is deemed to be of low significance.

3. Policy and Legislative Compliance

The report complies with the provisions to exclude the public from the whole or any part of the proceedings of any meeting as detailed in sections 47 and 48 of the Local Government Official Information Act 1987.

4. Other Considerations

Being a purely administrative matter; Community Views, Māori Impact Statement, Financial Implications, and Implementation Issues are not applicable.